Cost and Management Accountıng (ENG) - Tüm Sorular

Ünite 1

Soru 1

Which of the following is wrong with cost accounting?

Seçenekler

A

Purpose of cost accounting is to find the cost of product or service.

B

Expense is the sacrifice, measured by the price paid or to be paid, to acquire goods or services.

C

Cost accounting can be defined as information a system.

D

Purpose of cost accounting is planning and controlling activities.

E

Purpose of cost accounting is decision-making process.

Açıklama:

The correct answer is B. Cost is the sacrifice, measured by the price paid or to be paid, to acquire goods or services. The expense is defined as a noun, a decrease in owners’ equity accompanying the decrease in net assets caused by selling goods or rendering services or by the passage of time.

Soru 2

Which of the following is not the benefit of unit cost information in making important marketing decisions?

Seçenekler

A

Determining the selling price of a product

B

Meeting competition

C

Biddingoncontracts

D

Provides information to external users.

E

Analyzing profitability

Açıklama:

The correct answer is D. Unit cost information is also helpful in making important marketing decisions such as:

- Determining the selling price of a product

- Meeting competition

- Biddingoncontracts

- Analyzing profitability.

Soru 3

Which of the following is one of the production costs?

Seçenekler

A

Direct labor cost

B

Period expenses

C

Period earnings

D

Marketing or selling expenses

E

Administrative expenses

Açıklama:

The correct answer to question is option A. Manufacturing (product) cost is grouped under three headings:

• Direct raw material cost

• Direct labor cost

• Manufacturing (factory) overhead cost

• Direct raw material cost

• Direct labor cost

• Manufacturing (factory) overhead cost

Soru 4

Which of the following is not accurate information about management accounting?

Seçenekler

A

Management accounting is the process of supplying the managers and employees in an organization with relevant information, both financial and nonfinancial.

B

Management accounting measures and reports financial information as well as other types of information.

C

Management accounting as an information system that serves information to their ‘clients’, namely the managers.

D

Management accounting provides information to internal users.

E

Management accounting provides information to external users.

Açıklama:

The correct answer is question E. Financial accounting focuses on external reporting that is directed by authoritative guidelines. Therefore, financial accounting provides information to external users.

Soru 5

In which of the following options have types of inventory of the manufacturing-sector organizations given exactly?

Seçenekler

A

Direct materials inventory, work-inprocess inventory, finished goods inventory

B

Direct materials inventory, work-inprocess inventory, finished goods inventory and goods

C

Direct materials inventory and goods

D

Direct materials inventory and work-inprocess inventory

E

Work-inprocess inventory and finished goods inventory

Açıklama:

Manufacturing-sector organizations typically have one or more of the following three types of inventory: Direct materials inventory, work-inprocess inventory, finished goods inventory.

Soru 6

In which financial statement is the cost of goods sold?

Seçenekler

A

Balance Sheet

B

Cash Flow Statement

C

Income Statement

D

Statement of Changes in Shareholders' Equity

E

Inventory Card

Açıklama:

The correct answer is C. The cost of goods sold is included in the income statement.

Soru 7

I. Not affected by changes in operating volume

II. Varies according to changes in the volume of operations.

Which of the following is the correct matching of the expressions given above?

II. Varies according to changes in the volume of operations.

Which of the following is the correct matching of the expressions given above?

Seçenekler

A

I- Mixed Costs

B

II-Fixed Cost

C

I-Variable Cost

D

I-Mixed Cost

E

I-Fixed Cost

Açıklama:

The correct answer is question E. Variable costs represent cost behavior that is directly related to changes in the volume of operations and increases when the volume of activity increases. Fixed costs, on the other hand, are defined as costs that are not affected by changes in operating volume, at least in the short run.

Soru 8

Under which group of raw materials is inventory, work in process inventory and finished goods inventory are shown under the balance sheet?

Seçenekler

A

Cash

B

Inventory

C

Fixed Assets

D

Intangible Assets

E

Cost of goods sold

Açıklama:

The correct answer is B. Raw materials is inventory, work in process inventory and finished goods inventory are shown under the inventory in the balance sheet.

Soru 9

Which of the following is not use of maccounting information system in decision making?

Seçenekler

A

Performance evaluation and control

B

Developing objectives and plans

C

Allocating resources

D

Providing useful financial information to external users

E

Determining costs and benefits

Açıklama:

The correct answer is D. Management accounting provides information to internal users. The areas of management accounting in decision-making can be explained in detail: Developing objectives and plans, performance evaluation and control, allocating resources, determining costs and benefits.

Soru 10

...................... is period expenses and recorded as an expense in the

current accounting period.

Which of the following should be brought to the space left above?

current accounting period.

Which of the following should be brought to the space left above?

Seçenekler

A

Manufacturing Cost

B

Direct raw material cost

C

Non-manufacturing Cost

D

Direct labor cost

E

Manufacturing (factory) overhead cost

Açıklama:

The correct answer is C. Direct raw material cost, direct labor cost, manufacturing (factory) overhead cost is manufacturing cost. Non-manufacturing cost is period expenses and recorded as an expense in the

current accounting period.

current accounting period.

Soru 11

I. Globalization,

II. Automatization and Industry 4.0 revolution,

III. Technological developments

Which of the above is among the changes that businesses have been exposed to recently?

II. Automatization and Industry 4.0 revolution,

III. Technological developments

Which of the above is among the changes that businesses have been exposed to recently?

Seçenekler

A

Only I

B

Only II

C

I and III

D

II and III

E

I, II and III

Açıklama:

Economic and technological changes in

recent years, many organizations, especially in

the manufacturing sector, have faced significant

changes in their business environment. These

challenges can be summarized under three

headings:

• Globalization,

• Automatization and Industry 4.0 revolution,

• Technological developments.

recent years, many organizations, especially in

the manufacturing sector, have faced significant

changes in their business environment. These

challenges can be summarized under three

headings:

• Globalization,

• Automatization and Industry 4.0 revolution,

• Technological developments.

Soru 12

Which of the following is a financial statement that concerns only internal users?

Seçenekler

A

Balance sheet

B

Income statement

C

Cash flow statement

D

Statement of Changes in Shareholders' Equity

E

Cost of sales table

Açıklama:

Financial accounting produces useful

financial information to external users. Whereas,

cost accounting and management accounting

provide information to internal users.

financial information to external users. Whereas,

cost accounting and management accounting

provide information to internal users.

Soru 13

I. Financial accounting

II. Cost accounting

III. Management accounting

Which of the above provides information for external users?

II. Cost accounting

III. Management accounting

Which of the above provides information for external users?

Seçenekler

A

Only I

B

Only III

C

I and II

D

II and III

E

I, II and III

Açıklama:

Financial accounting produces useful

financial information to external users. Whereas,

cost accounting and management accounting

provide information to internal users.

financial information to external users. Whereas,

cost accounting and management accounting

provide information to internal users.

Soru 14

Which of the following relates to the provision of appropriate information for decision-making, planning, controlling and performance evaluation?

Seçenekler

A

Financaial accounting

B

General accounting

C

Management accounting

D

Cost accounting

E

Creative accounting

Açıklama:

Management accounting relates to the provision of appropriate information for decision-making, planning, controlling and performance evaluation.

Soru 15

I. To find the cost of product or service

II. Planning and controlling activities

III. Decision-making process

Which of the above is one of the objectives of cost accounting?

II. Planning and controlling activities

III. Decision-making process

Which of the above is one of the objectives of cost accounting?

Seçenekler

A

Only I

B

Only II

C

I and III

D

II and III

E

I, II and III

Açıklama:

Cost accounting can be defined as a system in which financial data regarding business transactions are collected, classified, recorded, evaluated and reported for the following three purposes:

• To find the cost of product or service,

• Planning and controlling activities,

• Decision-making process.

• To find the cost of product or service,

• Planning and controlling activities,

• Decision-making process.

Soru 16

Which of the following is included in the "Determining Product Costs and Pricing" purpose of cost accounting?

Seçenekler

A

Determining the selling price of a product

B

Meeting competition

C

Bidding on contracts

D

Assigning responsibility

E

Analyzing profitability

Açıklama:

Assigning responsibility takes place in planning and conrtol.

Soru 17

What is the definition of "A decrease in owners’ equity attendant the decrease in net assets caused by selling goods or provide services"?

Seçenekler

A

Cost

B

Expense

C

Income

D

Loss

E

Revenue

Açıklama:

The expense is defined as a noun, a decrease in owners’ equity attendant the decrease in net assets caused by selling goods or provide services.

Soru 18

What is the definition of "A resource sacrificed or forfeit to achieve a specific objective"?

Seçenekler

A

Cost

B

Expense

C

Loss

D

Income

E

Revenue

Açıklama:

Cost is a resource sacrificed or forfeit to achieve a specific objective.

Soru 19

I. Direct raw material cost

II. Direct labor cost

III. Manufacturing (factory) overhead cost

Which of the above is included in manufacturing costs?

II. Direct labor cost

III. Manufacturing (factory) overhead cost

Which of the above is included in manufacturing costs?

Seçenekler

A

Only I

B

Only III

C

I and II

D

II and III

E

I, II and III

Açıklama:

Manufacturing (product) cost is grouped under three headings:

• Direct raw material cost

• Direct labor cost

• Manufacturing (factory) overhead cost

• Direct raw material cost

• Direct labor cost

• Manufacturing (factory) overhead cost

Soru 20

Which of the following is not in key qualities of management accounting?

Seçenekler

A

Relevance

B

Reliability

C

Comparability

D

Accountability

E

Understandability

Açıklama:

Management accounting information system has many key qualities. These are:

- Relevance

- Reliability

- Comparability

- Understandability

Soru 21

-To find the cost of product or service

-Planning and controlling activities

-Decision-making process

What is the name of the system in which financial data regarding business transactions are collected, classified, recorded, evaluated and reported for the three purposes above?

-Planning and controlling activities

-Decision-making process

What is the name of the system in which financial data regarding business transactions are collected, classified, recorded, evaluated and reported for the three purposes above?

Seçenekler

A

Cost accounting

B

Manufacturing costs

C

Control

D

Planning

E

Pricing

Açıklama:

Cost accounting can be defined as a system in which financial data regarding business transactions are collected, classified, recorded, evaluated and reported for the following three purposes:

• To find the cost of product or service,

• Planning and controlling activities,

• Decision-making process.

• To find the cost of product or service,

• Planning and controlling activities,

• Decision-making process.

Soru 22

I. Determining the selling price of a product

II. Meeting competition

III. Bidding on contracts

IV. Analyzing profitability

Which of the above are among the important marketing decisions in which unit cost information is helpful?

II. Meeting competition

III. Bidding on contracts

IV. Analyzing profitability

Which of the above are among the important marketing decisions in which unit cost information is helpful?

Seçenekler

A

I and II

B

III and IV

C

I, II and III

D

II, III and IV

E

I, II, III and IV

Açıklama:

All of them are among the important marketing decisions in which unit cost information is helpful.

Soru 23

What is the name of the process of establishing objectives or goals for the business and calculating the means by which they will be met?

Seçenekler

A

Control

B

Planning

C

Management Accounting

D

Determining Product Costs

E

Pricing

Açıklama:

Planning is the process of establishing objectives or goals for the business and calculating the means by which they will be met.

Soru 24

I. Assigning Responsibility

II. Periodically Measuring and Comparing Results

III. Taking Necessary Corrective Action

Which of the steps above are necessary for achieving effective control?

II. Periodically Measuring and Comparing Results

III. Taking Necessary Corrective Action

Which of the steps above are necessary for achieving effective control?

Seçenekler

A

Only I

B

Only III

C

I and II

D

II and III

E

I, II and III

Açıklama:

All of them are necessary for achieving effective control.

Soru 25

What is the name of resource sacrificed or forfeit to achieve aspecific objective?

Seçenekler

A

Accounting

B

Function

C

Cost

D

Control

E

Planning

Açıklama:

Cost is a resource sacrificed or forfeit to achieve a specific objective.

Soru 26

What is the collection of cost data in some organized way by means of an accounting system?

Seçenekler

A

Cost assignment

B

Manufacturing overhead costs

C

Direct costs

D

Cost accumulation

E

Indirect costs

Açıklama:

Cost accumulation is the collection of cost data in some organized way by means of an accounting system.

Soru 27

What is the name of the general term that includes both tracing accumulated costs that have a direct relationship to a cost object and allocating accumulated costs that have an indirect relationship to a cost object?

Seçenekler

A

Cost accumulation

B

Cost assignment

C

Direct costs

D

Indirect costs

E

Period costs

Açıklama:

Cost assignment is a general term that includes both tracing accumulated costs that have a direct relationship to a cost object and allocating accumulated costs that have an indirect relationship to a cost object.

Soru 28

Which of the following is recognized as an expense in the period in which they are consumed and transferred to the income statement?

Seçenekler

A

Non-manufacturing expense

B

Period expense

C

Administrative expense

D

Operating expense

E

Selling expense

Açıklama:

Period expenses are recognized as an expense in the period in which they are consumed and transferred to the income statement.

Soru 29

What is the name of the costs that are directly identified with a cost object?

Seçenekler

A

Direct costs

B

Indirect costs

C

Manufacturing costs

D

Period costs

E

The manufacturing overhead costs

Açıklama:

Direct costs: These are the costs that are directly identified with a cost object.

Soru 30

Which of the following is a price that can be completely assigned to the production of specific goods or services?

Seçenekler

A

Indirect cost

B

Manufacturing overhead cost

C

Direct cost

D

Period Cost

E

Direct labor cost

Açıklama:

A direct cost is a price that can be completely assigned to the production of specific goods or services.

Soru 31

What is the name of the costs that are not directly identified with a cost object?

Seçenekler

A

Direct costs

B

Indirect costs

C

Manufacturing costs

D

Period costs

E

The manufacturing overhead costs

Açıklama:

Indirect costs: These are the costs that are not directly identified with a cost object.

Soru 32

I. Relevance

II. Reliability

III. Comparability

IV. Understandability

Which of the above are among the key qualities of management accounting information system?

II. Reliability

III. Comparability

IV. Understandability

Which of the above are among the key qualities of management accounting information system?

Seçenekler

A

I and II

B

III and IV

C

I, II and III

D

II, III and IV

E

I, II, III and IV

Açıklama:

All of them are among the key qualities of management accounting information system.

Soru 33

Which of the following represent cost behavior that is directly related to changes in the volume of operations and increases when the volume of activity increases and is zero?

Seçenekler

A

Fixed costs

B

Semi-fixed costs

C

Semi-variable costs

D

Variable costs

E

Manufacturing Costs

Açıklama:

Variable costs represent cost behavior that is directly related to changes in the volume of operations and increases when the volume of activity increases and is zero.

Soru 34

I. Raw material and supplies inventory

II. Work-in-process inventory

III. Finished goods inventory

Which of the items above are important inventory items in manufacturing organizations?

II. Work-in-process inventory

III. Finished goods inventory

Which of the items above are important inventory items in manufacturing organizations?

Seçenekler

A

Only I

B

Only III

C

I and II

D

II and III

E

I, II and III

Açıklama:

There are three important inventory items in manufacturing organizations:

1. Raw material and supplies inventory

2. Work-in-process inventory

3. Finished goods inventory

1. Raw material and supplies inventory

2. Work-in-process inventory

3. Finished goods inventory

Soru 35

Which of the following is transferred to the related asset account on the balance sheet when the product is completed?

Seçenekler

A

Inventoriable cost

B

Cost of goods sold

C

Product cost

D

Service cost

E

Period cost

Açıklama:

Inventoriable costs are transferred to the related asset account on the balance sheet when the product is completed.

Soru 36

Which of the key qualities of management accounting information system is related to the its having the ability to influence decisions?

Seçenekler

A

Reliability

B

Comparability

C

Understandability

D

Quality

E

Relevance

Açıklama:

Management accounting information system has many key qualities. These are (Atrill and McLaney, 2009: 17-18): • Relevance. Management accounting informationmust havethe ability to influence decisions

Soru 37

Which of the following will enable managers to identify changes in the business over time?

Seçenekler

A

Relevance

B

Comparability

C

Reliability

D

Quality

E

Understandability

Açıklama:

Comparability: This quality will enable managers to identify changes in the business over time.

Soru 38

What is the first step of a management accounting information system?

Seçenekler

A

Information evaluation

B

Information reporting

C

Information analysis

D

Information identification

E

Information recording

Açıklama:

There are four following stages of a management accounting information system. In the first stage, the information is defined and recorded in the other stage, in short, the first two stages are related to the preparation of the information. The third stage is the analysis of the information and the final stage is the reporting of the information. The last two stages emerge as the use of collected information.

Soru 39

What are the costs of purchasing the goods that are resold in the same form for merchandising-sector organizations?

Seçenekler

A

Product costs

B

Direct raw material costs

C

Inventoriable costs

D

Semi-fixed costs

E

Semi-variable costs

Açıklama:

For merchandising-sector organizations, inventoriable costs are the costs of purchasing the goods that are resold in the same form.

Soru 40

Which of the following accounting information users need management and cost accounting information?

Seçenekler

A

Managers

B

Shareholders

C

Creditors

D

Goverment

E

Banks

Açıklama:

The correct answer to question is option A. The users of accounting information can be divided into two categories. Internal parties within the organization such as employers, managers, workers and external parties such as shareholders, creditors, goverment and banks outside the organization. Financial accounting produces useful financial information to external users. Whereas, cost accounting and management accounting provide information to internal users.

Soru 41

I. Planning

II. Decision making

III. Controlling process within the organization

Which of the following types of accounting are listed above?

II. Decision making

III. Controlling process within the organization

Which of the following types of accounting are listed above?

Seçenekler

A

Financial Accounting

B

Corporate Accounting

C

Government Accounting

D

Bank Accounting

E

Cost and Management Accounting

Açıklama:

The correct answer is question E. The role of cost accounting and management accounting have been more strategic in decision making, planning and controlling process within the organization.

Soru 42

..................... is a resource sacrificed or forfeit to achieve a specific objective.

Which of the following should be brought to the space left above?

Which of the following should be brought to the space left above?

Seçenekler

A

Expense

B

Cost

C

Revenue

D

Profit

E

Expenditure

Açıklama:

The correct answer is B. Cost is a resource sacrificed or forfeit to achieve a

specific objective.

specific objective.

Soru 43

Which of the following is directly recognized as an expense without being included in the manufacturing cost?

Seçenekler

A

Direct raw material cost

B

Direct labor cost

C

Manufacturing (factory) overhead cost

D

Marketing or selling expenses

E

Conversion costs

Açıklama:

The correct answer is D. Marketing or selling expenses are recognized as period expense.

Soru 44

Which of the following is not one of the objectives of cost accounting?

Seçenekler

A

Determination of the cost of the product or service produced

B

Helping to make a budget for the future

C

Organize general purpose financial statements for external users

D

Planning and controlling activities

E

Decision-making process

Açıklama:

The correct answer is C. The preparation of general purpose financial statements is one of the purposes of financial accounting.

Soru 45

Which of the following is an example of costs that can be completely assigned to the production of specific goods or services?

Seçenekler

A

Depreciation Expenses

B

Direct labor cost

C

Manufacturing (factory) overhead cost

D

Marketing or selling expenses

E

Administrative expenses

Açıklama:

The correct answer is B. Direct raw material cost and direct labor cost is a costs that can be completely assigned to the production of specific goods or services. Manufacturing (factory) overhead cost are assigned to the product or service cost using the distribution key.

Soru 46

I. Property taxes

II. Direct material cost

III. Rent expense

Which of the above-listed costs are fixed costs?

II. Direct material cost

III. Rent expense

Which of the above-listed costs are fixed costs?

Seçenekler

A

I and II

B

II and III

C

I, II and III

D

I and III

E

Only III

Açıklama:

The correct answer is D. Direct material cost is changes in the volume of operations and increases when the volume of activity increases and is zero.

Soru 47

I. Globalization

II. Automatization and Industry 4.0 revolution

III. Technological developments

Which of the above affects the business enviroment?

II. Automatization and Industry 4.0 revolution

III. Technological developments

Which of the above affects the business enviroment?

Seçenekler

A

Only I

B

Only II

C

I and III

D

II and III

E

I, II and III

Açıklama:

Economic and technological changes in recent years, many organizations, especially in the manufacturing sector, have faced significant changes in their business environment. These challenges can be summarized under three headings:

• Globalization,

• Automatization and Industry 4.0 revolution,

• Technological developments

• Globalization,

• Automatization and Industry 4.0 revolution,

• Technological developments

Soru 48

..................................., inventoriable costs are the costs of purchasing the goods that are resold in the same form.

Which of the following should be brought to the space left above?

Which of the following should be brought to the space left above?

Seçenekler

A

Tourism sector organizations

B

Educational sector organizations

C

Service-sector organizations

D

Merchandising-sector organizations

E

Manufacturing-sector organizations

Açıklama:

The correct answer is D. For merchandising-sector organizations, inventoriable costs are the costs of purchasing the goods that are resold in the same form. Manufacturing-sector organizations, all manufacturing costs are inventoriable costs. In service-sector organizations, there are no inventoriable costs, there are only service costs. Tourism sector and educational sector organizations are service-sector organizations.

Soru 49

I. To find the price of product or service

II. Planning and controlling activities

III. Decision-making process

Which of the above is/are takes place in the main purposes of cost accounting?

II. Planning and controlling activities

III. Decision-making process

Which of the above is/are takes place in the main purposes of cost accounting?

Seçenekler

A

Only I

B

Only II

C

I and III

D

II and III

E

I, II and III

Açıklama:

Cost accounting can be defined as a system in which financial data regarding business transactions are collected, classified, recorded, evaluated and reported for the following three purposes:

• To find the cost of product or service, (NOT THE PRICE OF PRODUCT/SERVICE)

• Planning and controlling activities,

• Decision-making process.

• To find the cost of product or service, (NOT THE PRICE OF PRODUCT/SERVICE)

• Planning and controlling activities,

• Decision-making process.

Soru 50

Which one of the following is not included in the benefits of unit cost information?

Seçenekler

A

Determining the selling price of a product

B

Meeting competition

C

Bidding on contracts

D

Analyzing profitability

E

Contact with customers

Açıklama:

Unit cost information is also helpful in making important marketing

decisions such as:

decisions such as:

- Determining the selling price of a product

- Meeting competition

- Bidding on contracts

- Analyzing profitability

Soru 51

Which of the following does the definition "A resource sacrificed or forfeit to achieve a specific objective" mean?

Seçenekler

A

Cost

B

Purchase

C

Profit

D

Loss

E

Income

Açıklama:

Cost is a resource sacrificed or forfeit to achieve a

specific objective.

specific objective.

Soru 52

Which of the following is incorrect information about cost flows and classifications in a manufacturing company?

Seçenekler

A

Cost of goods sold is showed to the balance sheet.

B

The finished products stand in the balance sheet until they are sold.

C

When raw materials are used in production, their costs are transferred to the Work in Process inventory account as direct materials.

D

Direct labor cost is added directly to Work in Process.

E

Raw materials purchases are recorded in the Raw Materials inventory account.

Açıklama:

The correct answer to question is option A. Cost of goods sold is showed to the income statement.

Soru 53

Which of the following is a direct cost?

Seçenekler

A

Zipper in pants

B

Button in the jacket

C

Flour in the bread

D

Glue in the book

E

Paper in the magazine

Açıklama:

A direct cost is a price that can be

completely assigned to the production

of specific goods or services. However,

indirect costs are costs that are not directly

responsible to a cost object.

completely assigned to the production

of specific goods or services. However,

indirect costs are costs that are not directly

responsible to a cost object.

Soru 54

Which of the following is not one of the area management accounting in decision-making?

Seçenekler

A

Allocating resources

B

Performance evaluation and control

C

Determining costs and benefits

D

Developing objectives and plans

E

Preparation of financial statements

Açıklama:

The correct answer is question E. The areas of management accounting in decision-making can be explained in detail:

- Developing objectives and plans

- Performance evaluation and control

- Allocating resources

- Determining costs and benefits.

Soru 55

Which of the following is an indirect cost?

Seçenekler

A

Flour in the cake

B

Fabric in the jacket

C

Orange in the fruit juice

D

Paper in the book

E

Button in the shirt

Açıklama:

Indirect costs: These are the costs that are not directly identified with a cost object. Example: Lease cost for the company building housing the editors of The X Sports magazine

Soru 56

I. Direct raw material cost

II. Direct labor cost

III. Manufacturing (factory) overhead cost

Which of the above takes place in the manufacturing costs?

II. Direct labor cost

III. Manufacturing (factory) overhead cost

Which of the above takes place in the manufacturing costs?

Seçenekler

A

Only I

B

Only II

C

I and III

D

II and III

E

I, II and III

Açıklama:

Manufacturing (product) cost is grouped under three headings:

• Direct raw material cost

• Direct labor cost

• Manufacturing (factory) overhead cost

• Direct raw material cost

• Direct labor cost

• Manufacturing (factory) overhead cost

Soru 57

Which of the following contains the costs at which all indirect costs associated with production are monitored?

Seçenekler

A

Direct raw material cost

B

Direct labor cost

C

Manufacturing overhead cost

D

Marketing or selling expenses

E

Administrative expenses

Açıklama:

The manufacturing overhead costs are the

costs at which all indirect costs associated

with production are monitored.

costs at which all indirect costs associated

with production are monitored.

Soru 58

Which of the following represents cost behavior that is directly related to changes in the volume of operations and increases when the volume of activity increases and is zero?

Seçenekler

A

Fixed costs

B

Variable costs

C

Mixed costs

D

Total costs

E

Overhead costs

Açıklama:

Variable costs represent cost behavior that is directly related to changes in the volume of operations

and increases when the volume of activity increases and is zero.

and increases when the volume of activity increases and is zero.

Soru 59

Which of the following can be defined as costs that are not affected by changes in operating volume at least in the short run?

Seçenekler

A

Variable costs

B

Mixed costs

C

Fixed costs

D

Overhead costs

E

Total costs

Açıklama:

Fixed costs are defined as costs that are not affected by changes in operating volume at least in the short run.

Ünite 2

Soru 1

Which one of the following costs are the costs of the material used in the product which can be easily traced?

Seçenekler

A

Indirect costs

B

Overhead costs

C

Direct material costs

D

Labour costs

E

Managerial costs

Açıklama:

Direct material costs are the costs of the material used in the product which can be easily traced.

Soru 2

Which one of the following costs are the costs that are related to the product but cannot be traced easily and also there may be some costs that are not included product, but they are consumed for the production purposes?

Seçenekler

A

Indirect costs

B

Direct material costs

C

Standard costs

D

Process costs

E

Actual costs

Açıklama:

Indirect costs are the costs that are related to the product but cannot be traced easily and also there may be some costs that are not included product, but they are consumed for the production purposes.

Soru 3

Which one of the following is not among the expenses for raw materials and supplies can be traced within a four-step approach?

Seçenekler

A

Determination of purchase costs

B

Documentation and recording process

C

Pricing the consumption

D

Determination of consumption

E

Determination of production

Açıklama:

Determination of production is not among the expenses for raw materials and supplies can be traced within a four-step approach.

Soru 4

Which one of the following is used for drawing materials from the warehouse?

Seçenekler

A

Inventory card

B

Raw material

C

Warehouse receipt document

D

Materials request slip

E

Economic order quantity

Açıklama:

Materials Request Slip is used for drawing materials from the warehouse.

Soru 5

XYZ Company purchased 2.000 pieces (a) raw material for 12.000 TL for shoe production. Company also paid 1.500 TL for insurance and 1.000 TL for custom fee. 4.000 of transportation fee belongs to the supplier community. Calculate the purchase cost of the material.

Seçenekler

A

13.000 TL

B

13.500 TL

C

14.500 TL

D

18.500 TL

E

22.000 TL

Açıklama:

Cost of the (a) raw material should be calculated as follows: Material cost + insurance + custom fee. 12.000 + 1.500 + 1.000 = 14.500 TL

Soru 6

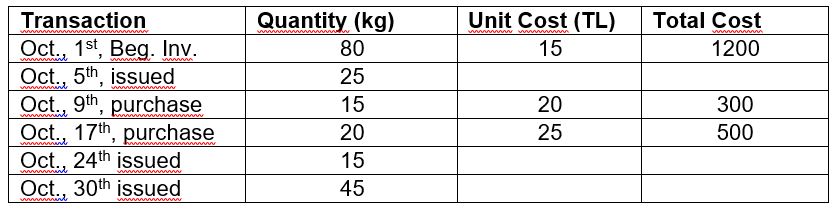

According to the FIFO method which one of the following is the cost of materials used for production?

According to the FIFO method which one of the following is the cost of materials used for production?Seçenekler

A

800 TL

B

900 TL

C

1.000 TL

D

1.200 TL

E

1.300 TL

Açıklama:

According to FIFO cost of the used material is: (25 x 15 TL) + (15 x 15 TL) + (40 x 15 TL) + (5 x 20 TL) = 1.300 TL

Soru 7

According to FIFO, calculate the cost of the material at the warehouse at the end of the period.

Seçenekler

A

700 TL

B

800 TL

C

900 TL

D

1.000 TL

E

1.100 TL

Açıklama:

According to FIFO, cost of the material at the warehouse should be calculated as follows: (15 x 20 TL) + (20 x 25 TL) = 800 TL

According to FIFO, cost of the material at the warehouse should be calculated as follows: (10 x 20 TL) + (20 x 25 TL) = 700 TL

According to FIFO, cost of the material at the warehouse should be calculated as follows: (10 x 20 TL) + (20 x 25 TL) = 700 TL

Soru 8

ABC Company produces heating spirals for refrigerators. The daily use of raw material is 350 kg. Lead time is 3 days and the management determined the safety stock level as 60 kg. Calculate the order point for the material.

Seçenekler

A

410 kg

B

700 kg

C

810 kg

D

1.110 kg

E

1.200 kg

Açıklama:

The daily usage of raw material is 350 kg. With the lead time taken into calculation (3 days), the total amount will be 1.050 kg (350x3). Safety stock is predetermined as 60 kg. So, when lead time and safety stock is considered 1.050 kg + 60 kg = 1.110 kg The company should reorder raw material when the material on hand decreases to 1.110 kg.

Soru 9

Which system classifies and ranks the inventories according to their respective costs or usages?

Seçenekler

A

Order cycling system

B

ABC system

C

Min-max plan

D

The two-bin system

E

VED analysis

Açıklama:

ABC system classifies and ranks the inventories according to their respective costs or usages.

Soru 10

In which inventory monitoring system companies classify their materials according to their “absence” costs?

Seçenekler

A

VED analysis

B

JIT system

C

The two-bin system

D

Min-max plan

E

ABC system

Açıklama:

In VED analysis, companies classify their materials according to their “absence” costs.

Soru 11

......................................... are the costs of the material used in the product which can be easily traced.

Which of the following should come to the dotted place according to the whole sentence?

Which of the following should come to the dotted place according to the whole sentence?

Seçenekler

A

İndirect costs

B

Direct material costs

C

Purchase cost

D

İnverntory flow cost

E

Continuity cost

Açıklama:

It should be Direct material cost

Soru 12

.................................are the costs that are related to the product but cannot be traced easily and also there may be some costs that are not included product, but they are consumed for the production purposes.

Which of the following should come to the dotted place according to the whole sentence?

Which of the following should come to the dotted place according to the whole sentence?

Seçenekler

A

Direct cost

B

İndirect cost

C

labor cost

D

Continuity cost

E

Purchase cost

Açıklama:

It should be indirect cost

Soru 13

The expenses for raw materials and supplies can be traced within a four-step approach.

Which one is not one of them ?

Which one is not one of them ?

Seçenekler

A

Documentation and recording process

B

Determination of purchase costs

C

Determination of consumption

D

Pricing the consumption

E

Determination of labor

Açıklama:

Determination of labor is not one of them

Soru 14

The companies use inventory flow assumptions in order to identify the cost of the material issued to production and the ending inventory.

Which one is not one of these assumptions?

Which one is not one of these assumptions?

Seçenekler

A

Specified Price

B

First-in-First-Out

C

Weighted Average Cost

D

Replacement Cost

E

Lowest-in-First-Out

Açıklama:

Lowest-in-First-Out is not one of them

Soru 15

....................................it is assumed that the material issued to the production is from the initial purchased material from the inventory.

Which of the following should come to the dotted place according to the whole sentence?

Which of the following should come to the dotted place according to the whole sentence?

Seçenekler

A

Last-in-First-Out

B

Highest-in-First-Out

C

Weighted Average Cost

D

Moving Average Cost

E

First-in-First-Out

Açıklama:

ıt should be First-in-First-Out

Soru 16

......................... an average price is calculated for a period by the relation between quantities and costs.The company calculates just one average price for the whole period.

Which of the following should come to the dotted place according to the whole sentence?

Which of the following should come to the dotted place according to the whole sentence?

Seçenekler

A

Specified Price

B

Replacement Cost

C

Standard Cost

D

Weighted Average Cost

E

Highest-in-First-Out

Açıklama:

It should be Weighted Average Cost

Soru 17

Inventories are one of the important assets of a company. Monitoring the inventories is as important as controlling them. There are several ways for monitoring the inventories.

Which one is not one of them ?

Which one is not one of them ?

Seçenekler

A

Min-Max Plan

B

The Two-Bin System

C

Order Cycling System

D

VED Analysis

E

JIB System

Açıklama:

JIB System is not one of them

Soru 18

......................................is one of the oldest inventory monitoring techniques. In this technique, a minimum and a maximum level is determined for each material in the inventory. When the inventory decreases to the minimum level, purchase order is prepared for the material to reach the maximum level.

Which of the following should come to the dotted place according to the whole sentence?

Which of the following should come to the dotted place according to the whole sentence?

Seçenekler

A

The Two-Bin System

B

Order Cycling System

C

ABC Analysis

D

VED Analysis

E

Min-Max Plan

Açıklama:

It should be Min-Max Plan

Soru 19

..................................... system is the purchase of materials just in time and just as the quantity needed. ......................... system is also used for production.

Which of the following should come to the dotted place according to the whole sentence?

Which of the following should come to the dotted place according to the whole sentence?

Seçenekler

A

JIT(Just in time) system

B

VED Analysis

C

Order Cycling System

D

The Two-Bin System

E

ABC System

Açıklama:

It should Just in time(JIT) System

Soru 20

Which of the following is not the raw materials of the product?

Seçenekler

A

Hardboard- Wardrobe

B

Leather-Shoes

C

Rubber- Tire

D

Grape- Wine

E

Paper-Table

Açıklama:

The correct answer is question E. The first item of the table is wood.

Soru 21

What is the monetary value of all materials used or consumed in production?

Seçenekler

A

Direct labor cost

B

Direct cost

C

İndirect cost

D

Direct material cost

E

Manufacturing overhead costs

Açıklama:

The correct answer is D. Direct material costs are the cost of the material used in the product which can be easily traced.

Soru 22

Which of the following is the correct information about direct material cost?

Seçenekler

A

It is not possible to directly determine how much the direct material cost is consumed for which product.

B

The manufacturing company cannot produce its own direct materials directly.

C

Raw material costs can be assigned directly to the product.

D

Raw materials do not form the structure of the product.

E

Raw material is not used directly during production.

Açıklama:

The correct answer is C.

Soru 23

Which of the following is not a inventory flow assumptions?

Seçenekler

A

First-in-First-Out (FIFO)

B

Weighted Average Cost

C

Factory cost method

D

Replacement Cost

E

Last-in-First-Out (LIFO)

Açıklama:

The correct answer is C. The companies use inventory flow assumptions in order to identify the cost of the material issued to production and the ending inventory. These assumptions are;

• Specified Price

• First-in-First-Out (FIFO)

• Last-in-First-Out (LIFO)

• Highest-in-First-Out (HIFO)

• Weighted Average Cost

• Moving Average Cost

• Replacement Cost

• Standard Cost

• Specified Price

• First-in-First-Out (FIFO)

• Last-in-First-Out (LIFO)

• Highest-in-First-Out (HIFO)

• Weighted Average Cost

• Moving Average Cost

• Replacement Cost

• Standard Cost

Soru 24

Which of the following cannot be inventory for a enterprises located across?

Seçenekler

A

Shirt- Textile Factory

B

Bread-Bakery

C

Peanut- Chocolate Factory

D

Board-Table Factory

E

Ink-Hotel

Açıklama:

The correct answer is question E. Hotels is a service business. Therefore they do not have stocks.

Soru 25

The inventory movements of the raw material in March of a manufacturing company are as follows:

According to this information, what is the cost of the material sent to production in March according to FIFO method?

| Date of Purchase | Transaction | Quantity (liters) | Unit Cost | Total Cost |

| 1 March | Beginning Inventory | 700 | 600 | |

| 12 March | purchase | 800 | 650 | 420.000 |

| 18 March | issued | 900 | 520.000 | |

| 23 March | purchase | 1.000 | 600 | 600.000 |

| 27 March | issued | 1.200 |

Seçenekler

A

1.320.000

B

1.336.000

C

1.600.000

D

1.273.000

E

1.300.000

Açıklama:

According to FIFO method:

18 March: 700X600= 420.000 and 200x650=130.000

27 March: 600x650=390.000 and 600x600=360.000

Inventory cost sent to total production= 1.300.000

18 March: 700X600= 420.000 and 200x650=130.000

27 March: 600x650=390.000 and 600x600=360.000

Inventory cost sent to total production= 1.300.000

Soru 26

The inventory movements of the raw material in March of a manufacturing company are as follows:

According to this information, what is end of period inventory cost in March according to FIFO method?

| Date of Purchase | Transaction | Quantity (liters) | Unit Cost | Total Cost |

| 1 March | Beginning Inventory | 700 | 600 | |

| 12 March | purchase | 800 | 650 | 420.000 |

| 18 March | issued | 900 | 520.000 | |

| 23 March | purchase | 1.000 | 600 | 600.000 |

| 27 March | issued | 1.200 |

Seçenekler

A

1.00.000

B

1.100.000

C

1.200.000

D

1.300.000

E

1.400.000

Açıklama:

At the end of the period, there are 600 unit inventory with a unit cost of 600 TL. End of period inventory cost is 1.200.000 TL

Soru 27

The inventory movements of the raw material in March of a manufacturing company are as follows:

According to this information, what is the cost of the material sent to production in March according to LIFO method?

| Date of Purchase | Transaction | Quantity (liters) | Unit Cost | Total Cost |

| 1 March | Beginning Inventory | 700 | 600 | |

| 12 March | purchase | 800 | 650 | 420.000 |

| 18 March | issued | 900 | 520.000 | |

| 23 March | purchase | 1.000 | 600 | 600.000 |

| 27 March | issued | 1.200 |

Seçenekler

A

900.000

B

1.000.000

C

1.150.000

D

1.200.000

E

1.300.000

Açıklama:

According to LIFO method:

18 March: 800X650=520.000 and 100X600=60.000

27 March: 1.000X600=600.000 and 200X600=120.000

Inventory cost sent to total production= 1.300.000

18 March: 800X650=520.000 and 100X600=60.000

27 March: 1.000X600=600.000 and 200X600=120.000

Inventory cost sent to total production= 1.300.000

Soru 28

The inventory movements of the raw material in March of a manufacturing company are as follows:

According to this information, what is the end of period inventory cost in March according to LIFO method?

| Date of Purchase | Transaction | Quantity (liters) | Unit Cost | Total Cost |

| 1 March | Beginning Inventory | 700 | 600 | |

| 12 March | purchase | 800 | 650 | 420.000 |

| 18 March | issued | 900 | 520.000 | |

| 23 March | purchase | 1.000 | 600 | 600.000 |

| 27 March | issued | 1.200 |

Seçenekler

A

230.000

B

240.000

C

250.000

D

260.000

E

270.000

Açıklama:

At the end of the period, there are 400 unit inventory with a unit cost of 600 TL. End of period inventory cost is 240.000 TL

Soru 29

The inventory movements of the raw material in March of a manufacturing company are as follows:

According to this information, what is the cost of the material sent to production in March according to Weighted Average Method?

| Date of Purchase | Transaction | Quantity (liters) | Unit Cost | Total Cost |

| 1 March | Beginning Inventory | 700 | 600 | |

| 12 March | purchase | 800 | 650 | 420.000 |

| 18 March | issued | 900 | 520.000 | |

| 23 March | purchase | 1.000 | 600 | 600.000 |

| 27 March | issued | 1.200 |

Seçenekler

A

1.295.910

B

1.300.000

C

1.425.000

D

1.500.000

E

1.530.000

Açıklama:

According to Weighted Average Method:

18 March : 900X626,6=563.940 TL

27 March: 1.200X609,975= 731.970 TL

Inventory cost sent to total production: 1.295.910 TL

18 March : 900X626,6=563.940 TL

27 March: 1.200X609,975= 731.970 TL

Inventory cost sent to total production: 1.295.910 TL

Soru 30

Which one is correct about direct material costs?

Seçenekler

A

Direct maretial costs cannot be traced easily.

B

Direct material costs are the cost of the material used in the product.

C

Direct materials can both be in the product and also they are used in the production process.

D

Direct materials are recognized as overhead costs when they are consumed.

E

Direct costs have to be allocated for the products produced.

Açıklama:

Direct costs are the costs that can be traced easily within the cost object. These aredirect material costs and direct labor costs. Direct material costs are the cost of the material used in the product which can be easily traced. For example, if the company can calculate the amount of carbon fiber material used in the frame of a carbon bicycle, then the carbon fiber used is assigned as direct material cost for the product.

Soru 31

__________ is used for drawing materials from the warehouse.

Seçenekler

A

Materials request slip

B

Warehouse receipt document

C

Balance column

D

Purchase cost

E

Periodic inventory systems

Açıklama:

Materials are drawn from the warehouse by the Materials Request Slip. This is the substantiating document that shows the inventory flow from the warehouse to the production plant. The slip carries information about the name, code and the quantity of the material, the name of the requester, sender and receiver and some other necessary information.

Soru 32

When the material is consumed, it is recorded into ______________ with amount, unit cost and total cost.

Seçenekler

A

Balance column

B

Issued column

C

Receipt column

D

Explanation column

E

Debit column

Açıklama:

When the company makes purchases the amount and the unit cost of the material is recorded into the Receipts column with the total cost. When the material is consumed, it is recorded into the Issues column with amount, unit cost and total cost. The difference between receipt and consumed is recorded as remaining material into the Balance column.

Soru 33

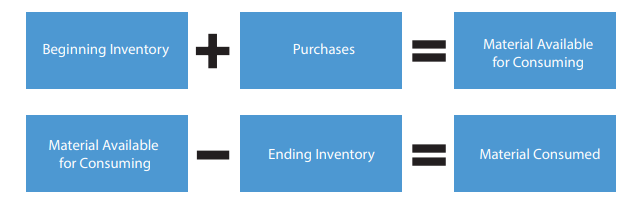

In periodic inventory system what gives us the materials that are consumed?

Seçenekler

A

Beginning inventory-Puchases=Material consumed

B

Beginning inventory-Ending inventory=Material consumed

C

Ending inventory+Begiinning inventory=Material used

D

Material available for consuming+Beginning inventory=Material consumed

E

Material available for consuming-Ending inventory=Materail consumed

Açıklama:

Soru 34

In which method it is assumed that the material issued to the production is from the initial purchased material from the inventory?

Seçenekler

A

FIFO method

B

LIFO metfod

C

HIFO

D

Specified method

E

Standard Method

Açıklama:

In FIFO method, it is assumed that the material issued to the production is from the initial purchased material from the inventory.

Soru 35

In which method an average price is calculated for a period by the relation between quantities and costs?

Seçenekler

A

FIFO

B

HIFO

C

LIFO

D

Weighted avarage method

E

Moving avarage method

Açıklama:

In weighted average method, an average price is calculated for a period by the relation between quantities and costs. The company calculates just one average price for the whole period. The average price is calculated as;

(Cost of Beginning Inventory+Cost of Receipts)/(Beginning Inventory+TotalQuantityof Receipts)

(Cost of Beginning Inventory+Cost of Receipts)/(Beginning Inventory+TotalQuantityof Receipts)

Soru 36

When the company wants to use a simple method for valuing its inventories, which method should it use?

Seçenekler

A

HIFO

B

Weighted avarage method

C

Moving avarage method

D

Replacement cost method

E

Standard cost method

Açıklama:

When the company wants to use a simple method for valuing its inventories, it is the standard cost method. Standard cost of a material is the cost that is predetermined by specific methods for a period that is affected by various factors like market prices, transportation costs, etc

Soru 37

___________ involves order point and economic order quantity.

Seçenekler

A

Investment control

B

Economic ordering quantity

C

Inventory planning

D

Safeguarding of materials

E

Segregating of duties

Açıklama:

The investment control consisting order point and the economic order quantity. Order point is an important issue for inventory policies. Over investment in materials yields to unproductivity so as lack of materials for production have the same effect on the company.

Soru 38

________ is used to determine when the materials should be replenished.

Seçenekler

A

VED analysis

B

Min-max system

C

ABC system

D

The two-bin system

E

Order cycling system

Açıklama:

The two-bin system is used to determine when the materials should be replenished. The first bin is for the materials that are being used in the production. The second bin is the substitute bin that is used in the lead time. When the materials in the first bin consumed, a new material order is given. Until the arrival of the new material, production is carried on with the materials in the second bin.

Soru 39

_________ is the purchase of materials just in time and just as the quantity needed.

Seçenekler

A

VED analysis

B

ABC system

C

JIT system

D

Order cycling system

E

The two-bin system

Açıklama:

JIT(Just-in-Time) system is the purchase of materials just in time and just as the quantity needed. Just-in-time system is also used for production. As a whole, JIT system aims not only decrease the inventory levels so as the costs related to inventory but also shortens production time, decrease the level of spoilage and defects, leaning the procedures of purchasing and simplifies the accounting transactions.

Ünite 3

Soru 1

Which of the following is one of the labour costs related to actual work?

Seçenekler

A

Week and Holiday Pays

B

Production and Efficiency Premium

C

Education and Training Payments

D

Health Payments

E

Severance Payments

Açıklama:

Labour costs related to actual work are:

- Basic pay

- Overtime pay

- Production and Efficiency Premium

Soru 2

Which of the following is not a labor cost related to legal or/and contractual enforcement or discretionary reasons?

Seçenekler

A

Overtime Pay

B

Night/Shift Premium

C

Holiday Pay

D

Social Security Premiums

E

Allowences

Açıklama:

Labor Costs related to Legal or/and Contractual Enforcement or Discretionary Reasons are:

- Week and Holiday Pays

- Overtime Premium

- Night/Shift Premium

- Social Welfare Contributions

- Health Payments

- Holiday Pay

- Allowances

- Education and Training Payments

- Severance Payments

- Social Security Premiums

- Unemployment Insurance Premiums

Soru 3

I.Time-based system

II. Piece based system

III. Premium based system

Which of the systems above ignores productivity?

II. Piece based system

III. Premium based system

Which of the systems above ignores productivity?

Seçenekler

A

Only I

B

Only II

C

Only III

D

I and II

E

I, II and III

Açıklama:

Under the time-based system, the important point is the time that employee spends at work. The measure of time can be the hour, day, week or month. Under this system, productivity is ignored, only time is considered.

Soru 4

In which account are direct labor costs incurred in a manufacturing company tracked?

Seçenekler

A

740 Cost of Production of Services

B

730 Manufacturing Overhead

C

723 Direct Labor Time Differences

D

720 Direct Labor Expenses

E

722 Direct Labor Wage Differences

Açıklama:

Direct labor costs incurred in a manufacturing company are tracked by 720 Direct Labor Expenses account.

Soru 5

Which account shows indirect labor costs incurred in a service company?

Seçenekler

A

721 Reflection Accounts for Direct Labor Expenses

B

722 Direct Labor Wage Differences

C

723 Direct Labor Time Differences

D

730 Manufacturing Overhead

E

740 Cost of Production of Services

Açıklama:

Direct labor costs incurred in a service company are tracked by 740 Cost of Production of Services account and indirect labor costs incurred in a service company are tracked again by 740 Cost of Production of Services account.

Soru 6

Which of the following refers to wages paid for an unproductive time caused by several ordinary and extraordinary reasons?

Seçenekler

A

Overtime Premium

B

Labor Costs

C

Idle Time

D

Payroll

E

Allowences

Açıklama:

Idle time refers to wages paid for an unproductive time caused by several ordinary and extraordinary reasons.

Soru 7

Which of the following terms refers to work which exceeds forty-five hours a week?

Seçenekler

A

Overtime work

B

Idle time

C

Labor cost

D

Time-based system

E

Premium based system

Açıklama:

Overtime work is defined in the Labor Act of Turkey Law no. 4857. Article 41 states that overtime work is work which exceeds forty-five hours a week.

Soru 8

Which is not one of the circumstances in which idle time may occur?

Seçenekler

A

Lack of orders

B

Machine or computer breakdowns

C

Poor scheduling

D

Need to increase output

E

Maintenance or repair of the machines

Açıklama:

Idle time is not related to a particular product; on the contrary, it is related to ordinary and/or extraordinary circumstances. Those circumstances can be lack of orders, machine or computer breakdowns, work delays, poor scheduling, maintenance or repair of the machines.

Soru 9

Which of the following terms refers to the process that includes calculating wages, withholding taxes and other deductions?

Seçenekler

A

Overtime work

B

Premium

C

Payroll

D

Idle time

E

Labor cost

Açıklama:

Payroll is not a salary or wage. Payroll or payroll register is a process. The process includes calculating wages, withholding taxes and other deductions.

Soru 10

Which of the following terms refers to the costs that are traceable to a specific cost object?

Seçenekler

A

Idle time

B

Overtime work

C

Premium

D

Indirect labor cost

E

Direct labor cost

Açıklama:

Costs that are traceable to a specific cost object are referred to as direct costs; costs that are not traceable to a specific cost object are referred to as indirect costs.

Soru 11

Which of the followings is not one of the elements of labor cost?

Seçenekler

A

Week and Holiday Pays

B

Employment Insurance Premiums

C

Education and Training Payments

D

Social Welfare Contributions

E

Production and Efficiency Premium

Açıklama:

ELEMENTS OF LABOR COSTS

Not Employment Insurance Premiums but Unemployment Insurance Premiums.

Not Employment Insurance Premiums but Unemployment Insurance Premiums.

Soru 12

Which of the followings is one of the labor costs related to actual work?

Seçenekler

A

Week and Holiday Pays

B

Overtime Premium

C

Night/Shift Premium

D

Production and Efficiency Premium

E

Social Welfare Contributions

Açıklama:

ELEMENTS OF LABOR COSTS

Production and Efficiency Premium is one of the Labor Costs Related to Actual Work

Production and Efficiency Premium is one of the Labor Costs Related to Actual Work

Soru 13

Which of the followings is a feature of "Direct Labor Costs"?

Seçenekler

A

It does not matter whether the employee is working for that company for full time or not.

B

They cover all payments done for indirect labor.

C

They refer to employees who are necessary for operations but who are not directly involved in the production or service process.

D

In a manufacturing plant, the supervisor that oversees operations but not involved in the production process is a part of direct labor cost.

E

In a restaurant payment for cleaning person that works in the kitchen but never works for cooking is a part of direct labor cost.

Açıklama:

Direct Labor Costs

It does not matter whether the employee is working for that company for full time or not. Direct labor comprises not only full- time employees but also part-time employees, temporary employees, and contractual employees as long as they are directly involved in operations.

It does not matter whether the employee is working for that company for full time or not. Direct labor comprises not only full- time employees but also part-time employees, temporary employees, and contractual employees as long as they are directly involved in operations.

Soru 14

Which of the followings refers to payments made to employees for regular work plus other payments such as premiums, allowances, social welfare payments and etc?

Seçenekler

A

Wage

B

Basic pay

C

Vested wage

D

Gross wage

E

Net Pay

Açıklama:

DETERMINING LABOR COSTS

Vested wage refers to payments made to employees for regular work plus other payments such as premiums, allowances, social welfare payments and etc.

Vested wage refers to payments made to employees for regular work plus other payments such as premiums, allowances, social welfare payments and etc.

Soru 15

Which of the followings refers to wage, which has not yet been object to any deduction due to legal enforcement?

Seçenekler

A

Wage

B

Basic wage

C

Vested wage

D

Gross wage

E

Net wage

Açıklama:

DETERMINING LABOR COSTS

Gross wage refers to wage, which has not yet been object to any deduction due to legal enforcement.

Gross wage refers to wage, which has not yet been object to any deduction due to legal enforcement.

Soru 16

Which of the followings is a process calculating wages, withholding taxes and other deductions?

Seçenekler

A

Payroll

B

Payment System

C

Indirect Labor Cost

D

Idle Time

E

Overtime Work

Açıklama:

Payroll Related Issues

Payroll is not a salary or wage. Payroll or payroll register is a process. The process includes calculating wages, withholding taxes and other deductions.

Payroll is not a salary or wage. Payroll or payroll register is a process. The process includes calculating wages, withholding taxes and other deductions.

Soru 17

Which of the followings refers to wages paid for an unproductive time caused by several ordinary and extraordinary reasons?

Seçenekler

A

Direct labor cost

B

Indirect Labor Cost

C

Payment System

D

Idle Time

E

Overtime Work

Açıklama:

Idle time refers to wages paid for an unproductive time caused by several ordinary and extraordinary reasons.

Soru 18

Which of the following statements is not true regarding labor costs?

Seçenekler

A

Labor is classified as direct labor and indirect labor.

B

Direct and indirect labor distinction depends on the employer.

C

If an employee directly involved in the production of goods and services, and then that employee is considered direct labor.

D

If an employee is not directly involved in the production, that employee is considered as indirect labor.

E

Direct labor cost includes wages paid to direct labor.

Açıklama:

Identify direct labor costs and indirect labor costs

Labor is classified as direct labor and indirect labor. This kind of distinction depends on the employee.

Labor is classified as direct labor and indirect labor. This kind of distinction depends on the employee.

Soru 19

Which of the following statements is true for the premium-based system?

Seçenekler

A

It focuses on the target, and the employee is paid a basic wage and premium for his/her efficient work.

B

It focuses on output and ignores the time spent at work.

C

Lack of this system is ignoring the competitiveness among employees to earn much more money.

D

Management of this system is difficult when the behavior employees are considered.

E

There are two main applications of this system; money accord and time accord.

Açıklama:

Identify direct labor costs and indirect labor costs

The premium-based system focuses on the target, and the employee is paid a basic wage and premium for his/her efficient work.

The premium-based system focuses on the target, and the employee is paid a basic wage and premium for his/her efficient work.

Soru 20

Which of the following statements is not true regarding the elements that are subject to labor costs?

Seçenekler

A

Wage is the main element of labor cost.

B

There is no basic wage paid to employees because of their normal work and some other additional payments.

C

Other than actual work of labor, employees are paid due to legal or/and contractual enforcement or discretionary reasons.

D

Wage is the amount of money to be paid in cash by an employer or by a third party to a person in return for work performed by him.

E

Payments are all related to the actual work of labor.

Açıklama:

Define the elements that are subject to labor costs

There is a basic wage paid to employees because of their normal work and some other additional payments such as overtime payment and premium payment for production and efficiency. They are all related to the actual work of labor.

There is a basic wage paid to employees because of their normal work and some other additional payments such as overtime payment and premium payment for production and efficiency. They are all related to the actual work of labor.

Soru 21

Which of the following excludes indirect labor cost?

Seçenekler

A

Holiday payments

B

Night/shift premium

C

Over-time premium

D

Wage

E

Social welfare contributions

Açıklama:

The correct answer is D. Indirect labor costs includes week and holiday payments, over-time premium, night/shift premium, social welfare contributions, health payments, holiday pay, allowances, education and training payments, severance payments, social security premiums and unemployment insurance premiums.

Soru 22

.................. are fixed payments to employees for their performance and productivity working on a monthly basis. However, ............. are payments to employees working on an hourly or daily basis.

Which of the following should be brought to the places left blank above?

Which of the following should be brought to the places left blank above?

Seçenekler

A

Salaries- wages

B

Holiday Pay-Wages

C

Salaries- Health Payments

D

Health Payments-Holiday Pays

E

Wages- Social Security Premiums

Açıklama:

The correct answer to question is option A. Salaries are fixed payments to employees for their performance and productivity working on a monthly basis. However, wages are payments to employees working on an hourly or daily basis.

Soru 23

I. Lack of this system is ignoring the competitiveness among employees to earn much more money.

II. It focuses on output.

III. It ignores the time spent at work.

Which of the following options is given above?

II. It focuses on output.

III. It ignores the time spent at work.

Which of the following options is given above?

Seçenekler

A

Piece-based system

B

Premium-based system

C

Money accord system

D

Time-based system

E

Time accord system

Açıklama:

The correct answer to question is option A. The piece-based system focuses on output and ignores the time spent at work. Lack of this system is ignoring the competitiveness among employees to earn much more money. There are two main applications of this piece-based system; money accord and time accord.

Soru 24

The definition of "the amount of money to be paid by the employer by a third party to a person in return for work performed by him" refers to which of the following?

Seçenekler

A

Wage

B

Salary

C

Cost

D

Income

E

Spending

Açıklama:

Wage is defined in the Labor Act of Turkey

Law no. 4857 by Article 32 as follows; “Wage

is, in general terms, the amount of money to

be paid in cash by an employer or by a third

party to a person in return for work performed

by him”

Law no. 4857 by Article 32 as follows; “Wage

is, in general terms, the amount of money to

be paid in cash by an employer or by a third

party to a person in return for work performed

by him”

Soru 25

Direct labor costs incurred in a manufacturing company are tracked by .......................

Which of the following accounts should be brought to the space left above?

Which of the following accounts should be brought to the space left above?

Seçenekler

A

730 Manufacturing Overhead account

B

740 Cost of Production of Services

C

720 Direct Labor Expenses account

D

722 Direct Labor Wage Differences

E

721 Reflection Accounts for Direct Labor Expenses

Açıklama:

The correct answer is C. Direct labor costs incurred in a manufacturing company are tracked by 720 Direct Labor Expenses account.

Soru 26

I. Basic Pay

II. Week and Holiday Pays

III. Social Security Premiums