Busıness Fınance II (ENG) - Tüm Sorular

Ünite 1

Soru 1

What is included in internal cash flow?

Seçenekler

A

Internal cash flow is generated from retained earnings and depreciation.

B

Internal cash flow is existing capital structure of the company,

C

Internal cash flow is availability of security.

D

These are generally in the forms of bank borrowing,

E

Internal cash flow is capital expenditures.

Açıklama:

Internal cash flow is generated from retained earnings and depreciation.

Soru 2

What is long term financing?

Seçenekler

A

The long-term financial requirements are the internal sources such as retained earning and depreciation provide financing to the corporate.

B

The long-term financial requirement means the finance needed to acquire land and building for business concern, purchase of plant and machinery and other fixed expenditures.

C

Long term financing is legal and tax issues.

D

Long term financing is bank lending capacity and relation with banks.

E

The Long term financing is based on the same principle as the revolving loans, but the limit of the credit is set as a debit of a company’s current account.

Açıklama:

The long-term financial requirement means the finance needed to acquire land and building for business concern, purchase of plant and machinery and other fixed expenditures. Long-term loans (payback period over 5 years, up to about 30 years such as for mortgage credits.

Soru 3

What happens when you have an overdraft?

Seçenekler

A

If you try to use your debit card when there is not enough money in your account to cover the transaction and your account can allow overdrawing to pay later without interest.

B

If your bank does pay your overdraft, you will not be charged a hefty fee for each overdraft transaction.

C

If the limit is overdrawn, the borrower pays a penalty interest rate.

D

Select the current account you would like to see the overdraft limit for.

E

Even if your current account is always in credit, it can be a good idea to have an overdraft facility arranged with your bank.

Açıklama:

The bank overdraft is based on the same principle as the revolving loans, but the limit of the credit is set as a debit of a company’s current account. If the limit is overdrawn, the borrower pays a penalty interest rate. Loans are granted by financial institutions after a client presents anapplication form.

Soru 4

How do bank fees work?

Seçenekler

A

Inflation will also affect interest rate levels.

B

Interest rate risk is the probability of a decline in the value of an asset resulting from unexpected fluctuations in interest rates.

C

Ask for accounts for older people or students.

D

Bank fees and charges are determined depending on the type of loan and on the lender.

E

Compare banks with similar features.

Açıklama:

Other fees and charges are determined depending on the type of loan and on the lender. Arrangement fees are commitment or administration charges payable to the lender to reserve the funds. Fees will vary depending on the complexity of the business, its size, and risk. Interest is charged and will vary dependingon risk of default.

Soru 5

What is differency between debt and equity?

Seçenekler

A

Debt is an ownership interest, equity represents an ownership of company.

B

The corporation’s payment of interest on debt is considered a cost of doing business but is not fully tax deductible.

C

One of the costs of issuing debt represents the possibility of financial success.

D

Equity can be in the form of term loans, debentures, and bonds, but dept can be in the form of shares and stock.

E

Debt holders are the creditors, whereas equityholders are the owners of the company.

Açıklama:

The main differences between debt and equity are the following:

• Debt is not an ownership interest in the firm. Creditors do not generally have votingpower.

• The corporation’s payment of interest ondebt is considered a cost of doing business and is fully tax deductible. Dividends paid to stockholders are not tax deductible.

• Unpaid debt is a liability of the firm. If itis not paid, the creditors can legally claim the assets of the firm. This action can result in liquidation or reorganization, two of the possible consequences of bankruptcy. Thus, one of the costs of issuing debt is the possibility of financial failure. This possibility does not arise when equity is issued.

• Debt is not an ownership interest in the firm. Creditors do not generally have votingpower.

• The corporation’s payment of interest ondebt is considered a cost of doing business and is fully tax deductible. Dividends paid to stockholders are not tax deductible.

• Unpaid debt is a liability of the firm. If itis not paid, the creditors can legally claim the assets of the firm. This action can result in liquidation or reorganization, two of the possible consequences of bankruptcy. Thus, one of the costs of issuing debt is the possibility of financial failure. This possibility does not arise when equity is issued.

Soru 6

What do you mean by optimal capital structure?

Seçenekler

A

Optimum capital structure is the capital structure at which the weighted average cost of capital is minimum and thereby the value of the firm is maximum.

B

An optimal capital structure is the best mix of debt.

C

A company's capital structure is arguably one of its most important choices.

D

The capital structure is how a firm finances its overall operations and growth by using different sources of funds.

E

The capital structure is defined as the careful balance between equity and debt.

Açıklama:

The decision to issue security in the form of debt or stock depends on the optimal capital structure of a corporate. The capitalization of a company can be defined as the balance sheet value of stocks and bonds outstanding. In this framework, capital structure refers to the kinds of securities and the proportionate amounts that make up capitalization.

Soru 7

What is a Eurobond?

Seçenekler

A

International bonds are issued in a country by a domestic entity.

B

A Eurobond is a bond issued in multiple countries but denominated in a single currency and those bonds have become an important way to raise capital for many international companies and governments.

C

A Eurobond is denominated in returnsas the company's stock other than that, of its country of issue.

D

Eurobond the stock market is unpredictable it is very easy to lose money by investing in the wrong stocks.

E

A Eurobond is an national bond that is denominated in a currency not native to the country where it is issued.

Açıklama:

A Eurobond is a bond issued in multiple countries but denominated in a single currency and those bonds have become an important way to raise capital for many international companies and governments. A Eurobond was once defined as a debt instrument underwritten by an international syndicate and offered for sale immediately in a number of countries. Eurobonds are issued outside the restrictions that apply to domestic offerings and are syndicated and traded mostly from London. However, trading can and does take place anywhere there are buyers and sellers.

Soru 8

what is common stock?

Seçenekler

A

A common stock is a representation of partial dept in a company, and is the dept of company.

B

If the company issues only common stock, with preferred shares then common stock equals the proffered shares.

C

A company's book value is equal to a company's assets minus its liabilities and found on the company's balance sheet.

D

Common stock, also named as equity shares, represents equity or an ownership position in a corporation.

E

The most common measure of a stock is the price/earnings ratio, which takes the share price and divides it by a company's annual net income.

Açıklama:

Common stock, also named as equity shares, represents equity or an ownership position in a corporation. The conceptual structure of the corporation assumes that shareholders elect directors who, in turn, hire management to carry out their directives. Shareholders, therefore, control the corporation through the right to elect the directors.

Soru 9

What is the concept of leasing?

Seçenekler

A

A lease is a contract outlining the terms under which one party agrees to give property owned by another party.

B

Known as the owner, buying of an asset and guarantees the seller the property owner or landlord, regular payments from the buyer for a specified number of months or years.

C

A lease agreement is a contract between a landlord and a buyer that covers the selling of property for long periods of time.

D

Vehicle using is the leasing of a motor vehicle for a fixed period of time at an agreed amount of money for the using.

E

A lease is a contractual agreement between a lessee and lessor establishing that the lessee has the right to use an asset and in return must make periodic payments to the lessor who is the owner of the asset.

Açıklama:

A lease is a contractual agreement between a lessee and lessor establishing that the lessee has the right to use an asset and in return must make periodic payments to the lessor who is the owner of the asset. The lessor is either the asset’s manufacturer or an independent leasing company.

Soru 10

How do floating rate bonds work?

Seçenekler

A

By the time the changing interest environment in the international financial markets, floating rate bonds (floaters) began to be issued in which, the coupon payments are adjustable.

B

A floating rate bond, where the bond has five years until maturity.

C

Some characteristics of the floaters have been developed in order to protect the investors.

D

A floating rate fund is a fund that invests in financial instruments paying but a fixed interest rate.

E

Floating rate notes are bonds that have a variable coupon, equal to a money market reference rate.

Açıklama:

The bonds conventionally have fixed interest payments up to maturity as calculated based on the fixed par value. However, by the time the changing interest environment in the international financial markets, floating-rate bonds (floaters) began to be issued in which, the coupon payments are adjustable. The adjustments are tied to an interest rate index such as the Treasury bill interest rate or the 30-year Treasury bond rate and the value of a floating-rate bond depends on exactly how the coupon payment adjustments are defined.

Soru 11

- Retained Earnings

- Depreciation

- Short-term Borrowings

- Long-term Debt

- Equity Finance

Seçenekler

A

I and II

B

I and III

C

II and III

D

I, II and IV

E

III, IV and V

Açıklama:

The financial management of a company requires the management of funds’ uses as well as optimizing the funding of those uses. The uses of cash flows are for net working capital and others and also for capital expenditures. In order to fund those uses, there exist two types of cash sources. Internal cash flow is generated from retained earnings and depreciation. External cash flow is generated from short-term borrowings and long-term debt and equity finance. As can also be understood from the information given, “short-term borrowings” , “long-term debt” and “equity finance” are the cash sources which external cash flow is generated from, so the correct answer is E.

Soru 12

- Debt Issuance

- Equity Finance

- Securitization

- Retained Earning

- Depreciation

Seçenekler

A

I and II

B

IV and V

C

I, II and III

D

III, IV and V

E

II, III, IV and V

Açıklama:

For funding investments and/or other cash uses by medium and long-term sources, the companies have four different alternatives. These are generally in the forms of bank borrowing, borrowing from special institutions, debt issuance and equity finance, securitization. Furthermore, depending on the peculiarities of the funding needs leasing can be another source of medium and long-term financing. Additionally, the internal sources such as Retained Earning and Depreciation provide financing to the corporate. As can also be understood from the information given “Retained Earning” and “Depreciation” are the internal sources which provide financing to the corporate, so the correct answer is B.

Soru 13

- Classical Loans

- Revolving Credits

- Bank Overdraft

- Project Loans

- Syndication Loans

Seçenekler

A

I and II

B

II and III

C

II and V

D

III and IV

E

IV and V

Açıklama:

According to the type of drawing and paying back, the loans are categorized as classical, revolving credits, bank overdraft, project loans, and syndication loans.

- With “classical” loans, after the drawing phase, the principal is paid gradually or by a single payment until a zero balance is achieved together with the interest for the period.

- With revolving credits, a limit of credit is set on the credit account of the borrower and both limits of credit and the due date are determined in a loan agreement. From concluding a loan contract till maturity date the borrower can draw the credit repeatedly within the limit.

- The bank overdraft is based on the same principle as the revolving loans, but the limit of the credit is set as a debit of a company’s current account. If the limit is overdrawn, the borrower pays a penalty interest rate. Loans are granted by financial institutions after a client presents an application form.

- The main medium and long term funding provided by banks are in the form of Project Finance. Project finance is the process of financing a specific economic unit that the sponsors create, in which creditors share much of the venture’s business risk and funding is obtained strictly for the project itself.

- Syndication loans are credits granted by a group of banks to a borrower. In a syndication loan, two or more banks agree jointly to make a loan to a borrower.

Soru 14

- Debt is not an ownership interest in the firm.

- The corporation’s payment of interest on debt is considered a cost of doing business and is fully tax deductible.

- Creditors do not generally have voting power.

- Dividends paid to stockholders are tax deductible.

- Unpaid debt is a liability of the firm.

Seçenekler

A

I and II

B

I and III

C

I, II and IV

D

I, II, III and V

E

II, III, IV and V

Açıklama:

Securities issued by corporations may be classified roughly as equity securities or debt securities. The main differences between debt and equity are the following:

- Debt is not an ownership interest in the Creditors do not generally have voting power.

- The corporation’s payment of interest on debt is considered a cost of doing business and is fully tax deductible. Dividends paid to stockholders are not tax deductible.

- Unpaid debt is a liability of the If it is not paid, the creditors can legally claim the assets of the firm. This action can result in liquidation or reorganization, two of the possible consequences of bankruptcy. Thus, one of the costs of issuing debt is the possibility of financial failure. This possibility does not arise when equity is issued.

Soru 15

- Desired Level of Leverage

- Nature of the business

- Size of the company

- Legal requirements

- Requirement of investors

Seçenekler

A

I and II

B

II and V

C

II, III and IV

D

I, III, IV and V

E

II, III, IV and V

Açıklama:

The following factors are considered while deciding the capital structure of the firm:

- Desired Level of Leverage: Financially, leverage refers to furnish the ability to use assets or funds with a fixed cost to increase the return to its shareholders. It is the basic and important factor, which affects the capital structure. It uses fixed-cost financing such as debt, equity and preference share capital and closely related to the overall cost of capital.

- Cost of Capital: Cost of capital is the main determining factor of the capital structure of a firm. Normally long-term finance such as equity and debt consist of fixed cost security issuance. When the cost of capital increases, the value of the firm will also decrease.

- Nature of the business: Use of fixed interest/dividend bearing finance depends upon the nature of the business. If the business consists of a long period of operation, it will apply for equity than debt, and it will reduce the cost of capital.

- Size of the company: It also affects the capital structure of a firm. If the firm belongs to a large scale, it can manage the financial requirements with the help of internal sources. Wheraes, if it is small size, they will go for external finance. It consists of a high cost of capital.

- Legal requirements: Some companies, such as banks are legally restricted to raise funds from some sources.

- Requirement of investors: In order to collect funds from a different type of investors, it will be appropriate for companies to issue different sources of securities.

Soru 16

- Debt securities are typically called notes, debentures, or bonds depending on their peculiarities.

- Issues with an original maturity of 10 years or less are often called bonds

- Longer-term issues are called notes.

- Long-term debt can be issued in two different forms, public-issue and privately-placed.

- Although the major terms and conditions are the same, under privately placed issues all of the bonds are sold to a single lender, not offered to the public.

Seçenekler

A

I and II

B

I, II and III

C

I, IV and V

D

I, II, IV and V

E

II, III, IV and V

Açıklama:

Debt securities are typically called notes, debentures, or bonds depending on their peculiarities. Despite the fact that a bond is a secured debt, it generally refers to all kinds of secured and unsecured debt. The difference between notes and bonds is the original maturity. Issues with an original maturity of 10 years or less are often called notes, longer-term issues are called bonds.

As can also be understood from the information given the statements “Debt securities are typically called notes, debentures, or bonds depending on their peculiarities.”, “Long-term debt can be issued in two different forms, public-issue and privately-placed.” and “Although the major terms and conditions are the same, under privately placed issues all of the bonds are sold to a single lender, not offered to the public.” are correct, so the correct answer is C.

The statements “Issues with an original maturity of 10 years or less are often called bonds” and “Longer-term issues are called notes.” are not correct. . Issues with an original maturity of 10 years or less are often called notes, longer-term issues are called bonds.

As can also be understood from the information given the statements “Debt securities are typically called notes, debentures, or bonds depending on their peculiarities.”, “Long-term debt can be issued in two different forms, public-issue and privately-placed.” and “Although the major terms and conditions are the same, under privately placed issues all of the bonds are sold to a single lender, not offered to the public.” are correct, so the correct answer is C.

The statements “Issues with an original maturity of 10 years or less are often called bonds” and “Longer-term issues are called notes.” are not correct. . Issues with an original maturity of 10 years or less are often called notes, longer-term issues are called bonds.

Soru 17

- The Par Value of a Bond

- The Face Value

- Common Stock

- Collateral

- Lease

Seçenekler

A

I and II

B

I and V

C

II and III

D

III and IV

E

IV and V

Açıklama:

The par value of a bond is almost always the same as the face value, and the terms are used interchangeably, so the correct answer is A.

Common stock, also named as equity shares, represnts equity or an ownership position in a corporation.

Collateral is a general term that frequently means securities that are pledged as security for payment of debt.

A lease is a contractual agreement between a lessee and lessor establishing that the lessee has the right to use an asset and in return must make periodic payments to the lessor who is the owner of the asset.

Common stock, also named as equity shares, represnts equity or an ownership position in a corporation.

Collateral is a general term that frequently means securities that are pledged as security for payment of debt.

A lease is a contractual agreement between a lessee and lessor establishing that the lessee has the right to use an asset and in return must make periodic payments to the lessor who is the owner of the asset.

Soru 18

- The basic terms of the bonds

- The total amount of bonds issued

- A description of property used as security

- The repayment arrangements

- The call provisions

- Details of the protective covenants

Seçenekler

A

I and II

B

I, II and III

C

III, IV and V

D

I, III, IV, V and VI

E

I, II, III, IV, V and VI

Açıklama:

The bond indenture is a legal document. It can run in several hundred pages it generally includes the following provisions:

- The basic terms of the bonds

- The total amount of bonds issued

- A description of property used as security

- The repayment arrangements

- The call provisions

- Details of the protective covenants

Soru 19

- No fixed dividend payment obligation

- Irredeemable

- Obstacles in Managemeent

- Limited Income to Investor

- Loss of Leverage Contributions

Seçenekler

A

I and II

B

II and III

C

I, III and IV

D

I, II, III and IV

E

II, III, IV and V

Açıklama:

Common stock is the most common security to provide finance for the corporate. This way of financing has the following disadvantages:

Irredeemable: Common stock cannot be redeemed during the lifetime of the company. Over capitalization is a very costly phenomenon financially so all companies must search for optimum capital structure.

Obstacles in management: Common stock holders can put obstacles in management by manipulation and organizing themselves. The managers may use their power in such ways that are against the wealth of the shareholders.

Limited income to investor: The investors who desire to invest in safe securities with a fixed income have no attraction for equity shares.

Loss of leverage contributions: When the company raises capital only with the help of equity, the company cannot take advantage of leverage

“Irredeemable”, “Obstacles in management”, “Limited income to investor” and “Loss of leverage contributions” are disadvantages of common stock, so the correct answer is E. “No fixed dividend payment obligation” is one of the advantages of common stock.

Advantages of common stock are as follows:

Permanent sources of finance: Common stock is a long-term permanent nature of sources of finance; hence, it can be used for long-term or fixed capital requirement of the business.

No fixed dividend payment obligation: The issuance of common stock does not create any obligation to pay a fixed rate of dividend. If the company earns a profit, owners are eligible for profit, they are eligible to get dividend otherwise, and they cannot claim any dividend from the company.

Lower cost of capital: Cost of capital is the major factor, which affects the value of the company. A company with a strong capital base can secure funding less costly as the capital base is considered as a buffer for risks buy the debtors.

Retained earnings: When the company have more share capital, it will be suitable for retained earning which is the fewer cost sources of finance while compared to other sources of finance.

Irredeemable: Common stock cannot be redeemed during the lifetime of the company. Over capitalization is a very costly phenomenon financially so all companies must search for optimum capital structure.

Obstacles in management: Common stock holders can put obstacles in management by manipulation and organizing themselves. The managers may use their power in such ways that are against the wealth of the shareholders.

Limited income to investor: The investors who desire to invest in safe securities with a fixed income have no attraction for equity shares.

Loss of leverage contributions: When the company raises capital only with the help of equity, the company cannot take advantage of leverage

“Irredeemable”, “Obstacles in management”, “Limited income to investor” and “Loss of leverage contributions” are disadvantages of common stock, so the correct answer is E. “No fixed dividend payment obligation” is one of the advantages of common stock.

Advantages of common stock are as follows:

Permanent sources of finance: Common stock is a long-term permanent nature of sources of finance; hence, it can be used for long-term or fixed capital requirement of the business.

No fixed dividend payment obligation: The issuance of common stock does not create any obligation to pay a fixed rate of dividend. If the company earns a profit, owners are eligible for profit, they are eligible to get dividend otherwise, and they cannot claim any dividend from the company.

Lower cost of capital: Cost of capital is the major factor, which affects the value of the company. A company with a strong capital base can secure funding less costly as the capital base is considered as a buffer for risks buy the debtors.

Retained earnings: When the company have more share capital, it will be suitable for retained earning which is the fewer cost sources of finance while compared to other sources of finance.

Soru 20

- Retained earnings are one of the least costly sources of finance since it does not involve any floatation cost as in the case of raising funds by issuing different types of securities.

- Retained earnings are most useful to expansion and diversification of the business activities.

- If the companies use equity finance they have to pay a dividend.

- When the company uses the retained earnings as the sources of finance for their financial requirements, the cost of capital is more expensive than the other sources of finance.

- Retained earnings provide opportunities for evasion of excessive tax in a company when it has a small number of shareholders.

Seçenekler

A

I and II

B

I, III and IV

C

III, IV and V

D

I, II, III and V

E

I, II, III, IV and V

Açıklama:

Retained earnings are another method of internal sources of finance and it is basically an accumulation of profits by a company for its expansion and diversification activities. The advantages of retained earnings are stated below:

The statement “When the company uses the retained earnings as the sources of finance for their financial requirements, the cost of capital is more expensive than the other sources of finance.” is not correct, because “when the company uses the retained earnings as the sources of finance for their financial requirements, the cost of capital is very cheaper than the other sources of finance.” Hence the value of the share will increase.

- Retained earnings are most useful to expansion and diversification of the business activities.

- Retained earnings are one of the least costly sources of finance since it does not involve any floatation cost as in the case of raising funds by issuing different types of securities.

- If the companies use equity finance they have to pay a dividend. Instead, if the companies use debt finance, they have to pay interest. However, if the company uses retained earnings as sources of finance, they need not pay any fixed obligation regarding the payment of dividend or interest.

- Retained earnings allow the financial structure to remain completely flexible. The company need not raise loans for further requirements if it has retained earnings.

- When the company uses the retained earnings as the sources of finance for their financial requirements, the cost of capital is very cheaper than the other sources of finance. Hence the value of the share will increase.

- Retained earnings provide opportunities for evasion of excessive tax in a company when it has a small number of shareholders.

The statement “When the company uses the retained earnings as the sources of finance for their financial requirements, the cost of capital is more expensive than the other sources of finance.” is not correct, because “when the company uses the retained earnings as the sources of finance for their financial requirements, the cost of capital is very cheaper than the other sources of finance.” Hence the value of the share will increase.

Soru 21

I. Capital Expenditures

II. Net working capital + other uses

III. Short-term debt

IV. Internal Cash Flow (Retained earnings + Depreciation)

Which of the above are among the "uses of cash flow"?

II. Net working capital + other uses

III. Short-term debt

IV. Internal Cash Flow (Retained earnings + Depreciation)

Which of the above are among the "uses of cash flow"?

Seçenekler

A

I and II

B

III and IV

C

I, II and III

D

II, III and IV

E

I, II, III and IV

Açıklama:

"Short-term debt" and "Internal Cash Flow (Retained earnings + Depreciation)" are among the sources of cash flow.

Soru 22

I. Long-term debt and equity

II. Short-term debt

III. Net working capital + other uses

IV. Internal Cash Flow (Retained earnings + Depreciation)

Which of the above are among the "sources of cash flow"?

II. Short-term debt

III. Net working capital + other uses

IV. Internal Cash Flow (Retained earnings + Depreciation)

Which of the above are among the "sources of cash flow"?

Seçenekler

A

I and II

B

III and IV

C

I, II and IV

D

II, III and IV

E

I, II, III and IV

Açıklama:

"Net working capital + other uses" are among the uses of cash flow.

Soru 23

In which bank loan type, after the drawing phase, the principal is paid gradually or by a single payment until a zero balance is achieved together with the interest for the period?

Seçenekler

A

Classical

B

Revolving credits

C

Bank overdraft

D

Project loans

E

Syndication loans

Açıklama:

With “classical” loans, after the drawing phase, the principal is paid gradually or by a single payment until a zero balance is achieved together with the interest for the period.

Soru 24

In which bank loan type, a limit of credit is set on the credit account of the borrower and both limits of credit and the due date are determined in a loan agreement?

Seçenekler

A

Classical

B

Revolving credits

C

Bank overdraft

D

Project loans

E

Syndication loans

Açıklama:

With revolving credits, a limit of credit is set on the credit account of the borrower and both limits of credit and the due date are determined in a loan agreement.

Soru 25

I. Debt is not an ownership interest in the firm.

II. The corporation’s payment of interest on debt is considered a cost of doing business and is fully tax deductible.

III. Unpaid debt is a liability of the firm.

Which of the above are among the main differences between debt and equity?

II. The corporation’s payment of interest on debt is considered a cost of doing business and is fully tax deductible.

III. Unpaid debt is a liability of the firm.

Which of the above are among the main differences between debt and equity?

Seçenekler

A

Only I

B

Only III

C

I and II

D

II and III

E

I, II and III

Açıklama:

All the things mentioned are among the main differences between debt and equity.

Soru 26

I. Desired Level of Leverage

II. Cost of Capital

III. Nature of the Business

IV. Size of the Company

Which of the above are among the factors determining capital structure?

II. Cost of Capital

III. Nature of the Business

IV. Size of the Company

Which of the above are among the factors determining capital structure?

Seçenekler

A

I and II

B

III and IV

C

I, II and IV

D

II, III and IV

E

I, II, III and IV

Açıklama:

All of the factors mentioned are among the factors determining capital structure.

Soru 27

I. The basic terms of the bonds

II. The total amount of bonds issued

III. The repayment arrangements

IV. Details of the protective covenants

Which of the above are among the provisions the bond indenture includes?

II. The total amount of bonds issued

III. The repayment arrangements

IV. Details of the protective covenants

Which of the above are among the provisions the bond indenture includes?

Seçenekler

A

I and II

B

III and IV

C

I, III and IV

D

II, III and IV

E

I, II, III and IV

Açıklama:

The bond indenture is a legal document. It can run in several hundred pages it generally includes the following provisions:

1. The basic terms of the bonds.

2. The total amount of bonds issued.

3. A description of property used as security.

4. The repayment arrangements.

5. The call provisions.

6. Details of the protective covenants.

1. The basic terms of the bonds.

2. The total amount of bonds issued.

3. A description of property used as security.

4. The repayment arrangements.

5. The call provisions.

6. Details of the protective covenants.

Soru 28

I. The maturity of the shares

II. Residual claim on income

III. Right to control

IV. Voting rights

Which of the above are among the important features of common stock?

II. Residual claim on income

III. Right to control

IV. Voting rights

Which of the above are among the important features of common stock?

Seçenekler

A

I and II

B

III and IV

C

I, III and III

D

II, III and IV

E

I, II, III and IV

Açıklama:

All the things mentioned are among the important features of common stock.

Soru 29

I. Permanent sources of finance

II. Irredeemable

III. No fixed dividend payment obligation

IV. Lower cost of capital

Which of the above are among the advantages of common stock?

II. Irredeemable

III. No fixed dividend payment obligation

IV. Lower cost of capital

Which of the above are among the advantages of common stock?

Seçenekler

A

I and II

B

III and IV

C

I, III and IV

D

II, III and IV

E

I, II, III and IV

Açıklama:

"Irredeemable" is among the disadvantages of common stock.

Soru 30

I. Obstacles in management

II. Loss of leverage contributions

III. Retained earnings

IV. Lower cost of capital

Which of the above are among the disadvantages of common stock?

II. Loss of leverage contributions

III. Retained earnings

IV. Lower cost of capital

Which of the above are among the disadvantages of common stock?

Seçenekler

A

I and II

B

III and IV

C

I, II and IV

D

II, III and IV

E

I, II, III and IV

Açıklama:

"Retained earnings" and "Lower cost of capital" are among the advantages of common stock.

Soru 31

Which of the following is an internal source of cash flow?

Seçenekler

A

Short-term debt

B

Long-term debt

C

Equity

D

Retained earnings

E

Capital expenditure

Açıklama:

Retained earnings are undistritued profits which become part of eqity and they are sources of cash flows to the company.

Soru 32

Which stakeholders have the highest priority in terms of claims on the income of the company?

Seçenekler

A

Common stockholders

B

Preferred stockholders

C

Bond holders

D

Employees

E

Customers

Açıklama:

Equity shareholders (common stockholders) have the right to get income left after paying for bondholders, as well as the fixed rate of dividend to preference shareholders. Thus, bondholders have the highest priority. Neither employees nor customers have claims on th income of the company.

Soru 33

The right which allows current shareholders to purchase their proportionate number of shares in any new stock offering in order to maintain their ownership in the company is referred to as .......

Seçenekler

A

Pre-emptive right

B

Right to vote

C

Right to control the management

D

Right to receive claims on the income

E

Right to receive claims on the assets

Açıklama:

Pre-emptive right offers the existing shareholders the first opportunity to purchase additional equity shares in proportion to their current holding capacity.

Soru 34

The following sources of financing are tax deductible except for...........

Seçenekler

A

Issuing bonds

B

Issuing shares of stock

C

Medium-term bank loans

D

Lon-term bank loans

E

Short-term bank loans

Açıklama:

Debt financing is tax deductible. Thus, except for issuing shares of stock, which is equity financing, the other sources given are tax deductible.

Soru 35

What is the name of the account managed by the bond trustee for the purpose of repaying the bonds?

Seçenekler

A

Treasury stock

B

Retained earnings

C

Coupon payments

D

Sinking fund

E

Savings account

Açıklama:

A sinking fund is an account managed by the bond trustee for the purpose of repaying the bonds.

Soru 36

Which of the following are accepted to be one of the main causes of the 2008-2009 financial crises?

Seçenekler

A

Government bonds

B

Callable bonds

C

Convertable bonds

D

Premium bonds

E

Securitized bonds

Açıklama:

Asset-backed, or securitized, bonds have been frequently used since the 2000s by the borrowers and for several years, there has been rapid growth in so-called subprime mortgage loans, which are mortgages made to individuals with less than top-quality credit. Those kinds of bonds are accepted to be one of the main causes of 2008-2009 financial crises.

Soru 37

Which type of bonds are issued in a foreign currency to the investors in the country?

Seçenekler

A

Yankee bonds

B

Samurai bonds

C

Rembrandt

D

Bulldog bonds

E

Eurobonds

Açıklama:

A Eurobond is usually denominated in a currency (or unit of account) that is foreign to a large number of buyers. The other choices give are foreign bonds. A foreign bond is similar to a domestic bond except that the issuer of the foreign bond is a foreign entity. Hence they are issued in the domestic currency of the country in which they are issued.

Soru 38

A bond with ............. attached, the buyers also receive the right to purchase a predetermined number of shares of stock of the company at a fixed price per share over the subsequent life of the bond.

Seçenekler

A

options

B

convertible feature

C

warrant

D

covenant

E

debenture

Açıklama:

For a bond with warrants attached, the buyers also receive the right to purchase a predetermined number of shares of stock of the company at a fixed price per share over the subsequent life of the bond.

Soru 39

Capital structure is a mix of the following sources of financing except for.....

Seçenekler

A

Short-term loans

B

Long-term loans

C

Preffered stock

D

Common stock

E

Debentures

Açıklama:

Capital structure is the mix of different sources of long-term sources such as equity shares, preference shares, debentures, long-term loans, and retained earnings. Hence, it does not inlude short-term loans.

Soru 40

Which of the following are used to reduce the tax burden and overall profitability of the company?

Seçenekler

A

Retained earnings

B

Depreciation funds

C

Emergency funds

D

Sinking funds

E

Saving accounts

Açıklama:

Depreciation funds are used to reduce the tax burden and overall profitability of the company

Soru 41

I. retained earnings

II. short-term borrowings

III. long-term debt

IV. depreciation

V. equity finance

Which of the cash sources above are used to generate funds for internal cash flows?

II. short-term borrowings

III. long-term debt

IV. depreciation

V. equity finance

Which of the cash sources above are used to generate funds for internal cash flows?

Seçenekler

A

I and II

B

I and III

C

I and IV

D

II and V

E

III and V

Açıklama:

The financial management of a company requires the management of funds’ uses as well as optimizing the funding of those uses. The uses of cash flows are for net working capital and others and also for capital expenditures. In order to fund those uses, there exist two types of cash sources. Internal cash flow is generated from retained earnings and depreciation. External cash flow is generated from short-term borrowings and long-term debt and equity finance. The correct answer is C.

Soru 42

In common stocks, what is the terms used to refer to the legal right of the existing shareholders?

Seçenekler

A

Pre-emptive right

B

Limited liability

C

Residual claims on assets

D

Right to control

E

Voting rights

Açıklama:

Pre-emptive right: Equity shareholders have pre-emptive rights. The pre-emptive right is the legal right of the existing shareholders. It is attested by the company in the first opportunity to purchase additional equity shares in proportion to their current holding capacity. The correct answer is A.

Soru 43

Which of the following is not true about revolving loans?

Seçenekler

A

With revolving credits, a limit of credit is set on the credit account of the borrower.

B

The limits of credit and the is determined in a loan agreement.

C

From concluding a loan contract till maturity date the borrower can draw the credit repeatedly within the limit.

D

The limit of the credit is set as a debit of a company’s current account if the limit is overdrawn.

E

The due date is determined in a loan agreement.

Açıklama:

With revolving credits, a limit of credit is set on the credit account of the borrower and both limits of credit and the due date are determined in a loan agreement. From concluding a loan contract till maturity date the borrower can draw the credit repeatedly within the limit. The bank overdraft is based on the same principle as the revolving loans, but the limit of the credit is set as a debit of a company’s current account. The correct answer is D.

Soru 44

Which of the following is not among the ways that a project finance creates value?

Seçenekler

A

decreasing the leverage ratios

B

reducing the costs of funding

C

maintaining the sponsor’s financial flexibility

D

reducing corporate taxes

E

improving risk management

Açıklama:

Project finance is the process of financing a specific economic unit that the sponsors create, in which creditors share much of the venture’s business risk and funding is obtained strictly for the project itself. Project finance creates value by reducing the costs of funding, maintaining the sponsor’s financial flexibility, increasing the leverage ratios, avoiding contamination risk, reducing corporate taxes, improving risk management, and reducing the costs associated with market imperfections. The correct answer is A.

Soru 45

In regards with the main differences between debt and equity, which of the following is true?

Seçenekler

A

Debt is an ownership interest in the firm.

B

In debt, creditors generally have voting power.

C

Payment of interest on debt is fully tax deductible.

D

Unpaid debt is a liability of the creditors.

E

One of the costs of issuing equity is the possibility of financial failure.

Açıklama:

The main differences between debt and equity are the following:

• Debt is not an ownership interest in the firm. Creditors do not generally have voting power.

• The corporation’s payment of interest on debt is considered a cost of doing business and is fully tax deductible. Dividends paid to stockholders are not tax deductible.

• Unpaid debt is a liability of the firm. If it is not paid, the creditors can legally claim the assets of the firm. This action can result in liquidation or reorganization, two of the possible consequences of bankruptcy. Thus, one of the costs of issuing debt is the possibility of financial failure. This possibility does not arise when equity is issued.

The correct answer is C.

• Debt is not an ownership interest in the firm. Creditors do not generally have voting power.

• The corporation’s payment of interest on debt is considered a cost of doing business and is fully tax deductible. Dividends paid to stockholders are not tax deductible.

• Unpaid debt is a liability of the firm. If it is not paid, the creditors can legally claim the assets of the firm. This action can result in liquidation or reorganization, two of the possible consequences of bankruptcy. Thus, one of the costs of issuing debt is the possibility of financial failure. This possibility does not arise when equity is issued.

The correct answer is C.

Soru 46

What is the term used to define the decrease in the value of an asset due to wear and tear, lapse of time, obsolescence, exhaustion and accident?

Seçenekler

A

Depreciation

B

Interest

C

Arrangement fees

D

Covenant compliance costs

E

Flotation costs

Açıklama:

Depreciation funds are the major part of internal sources of finance, which is used to meet the working capital requirements of the business concern. Depreciation means a decrease in the value of an asset due to wear and tear, lapse of time, obsolescence, exhaustion and accident. Generally, depreciation is changed against fixed assets of the company at a fixed rate for every year. The correct answer is A.

Soru 47

Which of the following is true about retained earnings?

Seçenekler

A

As a source of finance, retained earnings include floatation costs.

B

When the retained earnings are used, companies need to pay both the interest and the dividend.

C

Retained earnings prevent the financial structure from remaining completely flexible.

D

They provide opportunities for evasion of excessive tax when it has a small number of shareholders.

E

In retained earnings, the cost of capital is much more expensive than other sources of finance.

Açıklama:

The advantages of retained earnings are stated below:

• Retained earnings are most useful to expansion and diversification of the business activities.

• Retained earnings are one of the least costly sources of finance since it does not involve any floatation cost as in the case of raising funds by issuing different types of securities.

• If the companies use equity finance they have to pay a dividend. Instead, if the companies use debt finance, they have to pay interest. However, if the company uses retained earnings as sources of finance, they need not pay any fixed obligation regarding the payment of dividend or interest.

• Retained earnings allow the financial structure to remain completely flexible. The company need not raise loans for further requirements if it has retained earnings.

• When the company uses the retained earnings as the sources of finance for their financial requirements, the cost of capital is very cheaper than the other sources of finance. Hence the value of the share will increase.

• Retained earnings provide opportunities for evasion of excessive tax in a company when it has a small number of shareholders.

The correct answer is D.

• Retained earnings are most useful to expansion and diversification of the business activities.

• Retained earnings are one of the least costly sources of finance since it does not involve any floatation cost as in the case of raising funds by issuing different types of securities.

• If the companies use equity finance they have to pay a dividend. Instead, if the companies use debt finance, they have to pay interest. However, if the company uses retained earnings as sources of finance, they need not pay any fixed obligation regarding the payment of dividend or interest.

• Retained earnings allow the financial structure to remain completely flexible. The company need not raise loans for further requirements if it has retained earnings.

• When the company uses the retained earnings as the sources of finance for their financial requirements, the cost of capital is very cheaper than the other sources of finance. Hence the value of the share will increase.

• Retained earnings provide opportunities for evasion of excessive tax in a company when it has a small number of shareholders.

The correct answer is D.

Soru 48

Which of the following is true about financial leases?

Seçenekler

A

Financial leases provide for maintenance and service by the lessor.

B

The lessee has the sole responsibility to make all payments.

C

The lessor has a right to renew the lease on expiration.

D

Generally, financial leases can be canceled easily.

E

Financial leases are partially amortized.

Açıklama:

Financial leases are basically a medium-term financing alternative referring to its basic characteristics indicated below:

• Financial leases do not provide for maintenance or service by the lessor.

• Financial leases are fully amortized.

• The lessee usually has a right to renew the lease on expiration.

• Generally, financial leases cannot be canceled. The lessee has the sole responsibility to make all payments.

The correct answer is B.

• Financial leases do not provide for maintenance or service by the lessor.

• Financial leases are fully amortized.

• The lessee usually has a right to renew the lease on expiration.

• Generally, financial leases cannot be canceled. The lessee has the sole responsibility to make all payments.

The correct answer is B.

Soru 49

Which of the following is an advantage of common stock?

Seçenekler

A

Being irredeemable

B

Obstacles in management

C

lack of fixed dividend payment obligation

D

Limited income to investor

E

Loss of leverage contributions

Açıklama:

Advantages of Common Stock Common stock is the most common security to provide finance for the corporate. This way of financing has the following advantages:

Permanent sources of finance: Common stock is a long-term permanent nature of sources of finance; hence, it can be used for long-term or fixed capital requirement of the business.

No fixed dividend payment obligation: The issuance of common stock does not create any obligation to pay a fixed rate of dividend. If the company earns a profit, owners are eligible for profit, they are eligible to get dividend otherwise, and they cannot claim any dividend from the company.

Lower cost of capital: Cost of capital is the major factor, which affects the value of the company. A company with a strong capital base can secure funding less costly as the capital base is considered as a buffer for risks buy the debtors.

Retained earnings: When the company have more share capital, it will be suitable for retained earning which is the fewer cost sources of finance while compared to other sources of finance.

The correct answer is C.

Permanent sources of finance: Common stock is a long-term permanent nature of sources of finance; hence, it can be used for long-term or fixed capital requirement of the business.

No fixed dividend payment obligation: The issuance of common stock does not create any obligation to pay a fixed rate of dividend. If the company earns a profit, owners are eligible for profit, they are eligible to get dividend otherwise, and they cannot claim any dividend from the company.

Lower cost of capital: Cost of capital is the major factor, which affects the value of the company. A company with a strong capital base can secure funding less costly as the capital base is considered as a buffer for risks buy the debtors.

Retained earnings: When the company have more share capital, it will be suitable for retained earning which is the fewer cost sources of finance while compared to other sources of finance.

The correct answer is C.

Soru 50

In common stocks, if the company is wound up, the ordinary or equity shareholders have the right to get the claims on assets. These rights are only available to the equity shareholders.

Which of the following terms is used to refer to this situation?

Which of the following terms is used to refer to this situation?

Seçenekler

A

The maturity of the shares

B

Right to control

C

Pre-emptive right

D

Residual claims on assets

E

Voting rigths

Açıklama:

Residual claims on assets: If the company is wound up, the ordinary or equity shareholders have the right to get the claims on assets. These rights are only available to the equity shareholders. The correct answer is D.

Soru 51

Which of the followings is not among the altenratives for funding investments and/or other cash uses by medium and long-term sources?

Seçenekler

A

Securitization.

B

Borrowing from special institutions.

C

Debt issuance and equity finance.

D

Trading of auto-issued bonds.

E

Bank borrowing.

Açıklama:

Page 3.

For funding investments and/or other cash uses by medium and long-term sources, the companies have four different alternatives. These are generally in the forms of bank borrowing, borrowing from special institutions, debt issuance and equity finance, securitization. Therefore, the correct option is D.

For funding investments and/or other cash uses by medium and long-term sources, the companies have four different alternatives. These are generally in the forms of bank borrowing, borrowing from special institutions, debt issuance and equity finance, securitization. Therefore, the correct option is D.

Soru 52

Which of the followings is one of the internal alternatives for the companies to fund their investments?

Seçenekler

A

Leasing.

B

Depreciation.

C

Securitization.

D

Debt issuance.

E

Equity finance.

Açıklama:

Page 3.

For funding investments and/or other cash uses by medium and long-term sources, the companies have four different alternatives. These are generally in the forms of bank borrowing, borrowing from special institutions, debt issuance and equity finance, securitization. Furthermore, depending on the peculiarities of the funding needs leasing can be another source of medium and long-term financing. Additionally, the internal sources such as Retained Earning and Depreciation provide financing to the corporate. Therefore, the correct option is B.

For funding investments and/or other cash uses by medium and long-term sources, the companies have four different alternatives. These are generally in the forms of bank borrowing, borrowing from special institutions, debt issuance and equity finance, securitization. Furthermore, depending on the peculiarities of the funding needs leasing can be another source of medium and long-term financing. Additionally, the internal sources such as Retained Earning and Depreciation provide financing to the corporate. Therefore, the correct option is B.

Soru 53

I. Legal and tax issues,

II. Availability of security,

III. Marginal benefit,

IV. Capital market depth.

Which of the ones listed above is among the important factors affecting the decision for finding resources for the companies to fund investments?

II. Availability of security,

III. Marginal benefit,

IV. Capital market depth.

Which of the ones listed above is among the important factors affecting the decision for finding resources for the companies to fund investments?

Seçenekler

A

I, II & III.

B

II, III & IV.

C

I, II & IV.

D

II & III.

E

I & IV.

Açıklama:

Page 3.

Some of the important factors affecting the decision amongst those alternatives are: • Peculiarities of the fund use (whether machinery or equipment purchase financing or construction, etc.)Some of the important factors affecting the decision amongst those alternatives are:

• Peculiarities of the fund use (whether machinery or equipment purchase financing or construction, etc.)

• Bank lending capacity and relation with banks,

• Availability of security,

• Existing capital structure of the company,

• Capital market depth,

• Financial climate (Boom or boost financial market conditions),

• Legal and tax issues,

• The approach of top management with regards to equity sharing.

Therefore, the correct option is C.

Some of the important factors affecting the decision amongst those alternatives are: • Peculiarities of the fund use (whether machinery or equipment purchase financing or construction, etc.)Some of the important factors affecting the decision amongst those alternatives are:

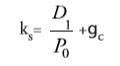

• Peculiarities of the fund use (whether machinery or equipment purchase financing or construction, etc.)

• Bank lending capacity and relation with banks,

• Availability of security,

• Existing capital structure of the company,

• Capital market depth,

• Financial climate (Boom or boost financial market conditions),

• Legal and tax issues,

• The approach of top management with regards to equity sharing.

Therefore, the correct option is C.

Soru 54

I. Short-term debt,

II. Long-term debt,

III. Depreciation,

IV. Retained earnings.

Which of the ones listed above is among the internal cash flow?

II. Long-term debt,

III. Depreciation,

IV. Retained earnings.

Which of the ones listed above is among the internal cash flow?

Seçenekler

A

I & II.

B

Only III.

C

II & IV.

D

I & IV.

E

III & IV.

Açıklama:

Page 3.

In order to fund those uses, there exist two types of cash sources. Internal cash flow is generated from retained earnings and depreciation. External cash flow is generated from short-term borrowings and long-term debt and equity finance. As a general principle, short-term uses are proposed to be financed by short-term sources and vice versa. Long-term uses of cash are basically for funding the future of the company by new investments. Therefore, the correct option is E.

In order to fund those uses, there exist two types of cash sources. Internal cash flow is generated from retained earnings and depreciation. External cash flow is generated from short-term borrowings and long-term debt and equity finance. As a general principle, short-term uses are proposed to be financed by short-term sources and vice versa. Long-term uses of cash are basically for funding the future of the company by new investments. Therefore, the correct option is E.

Soru 55

Which of the followings is an example of long-term loans?

Seçenekler

A

Mortgage.

B

Payday loans.

C

Credit card debts.

D

Revolving credits.

E

Overdraft.

Açıklama:

Page 3.

The funding provided by the banks are classified into short-term loans (payback period up to 1 year), medium-term loans (payback period 1 to 5 years) and long-term loans (payback period over 5 years, up to about 30 years such as for mortgage credits. Therefore, the correct option is A.

The funding provided by the banks are classified into short-term loans (payback period up to 1 year), medium-term loans (payback period 1 to 5 years) and long-term loans (payback period over 5 years, up to about 30 years such as for mortgage credits. Therefore, the correct option is A.

Soru 56

I. Surety for a person.

II. Feasibility,

III. Pledge,

IV. Leasing.

Which of the factors listed above is assessed by the banks while deciding on a loan?

II. Feasibility,

III. Pledge,

IV. Leasing.

Which of the factors listed above is assessed by the banks while deciding on a loan?

Seçenekler

A

I, II & III.

B

Only I.

C

II, III & IV.

D

Only II.

E

I, III & IV.

Açıklama:

Page 4.

Loans are granted by financial institutions after a client presents an application form. Before deciding about providing the loan, financial institutions consider all details of the client’s financial position, the feasibility of their business plans, and they require securing the loan with real estate (pledge), backing it by a third person (surety for a person), by a bank guarantee etc. Therefore, the correct option is A.

Loans are granted by financial institutions after a client presents an application form. Before deciding about providing the loan, financial institutions consider all details of the client’s financial position, the feasibility of their business plans, and they require securing the loan with real estate (pledge), backing it by a third person (surety for a person), by a bank guarantee etc. Therefore, the correct option is A.

Soru 57

Which of the followings is the main form that banks provide medium and long term funding?

Seçenekler

A

Leasing.

B

Project finance.

C

Classical loans.

D

Overdraft.

E

Revolving credits.

Açıklama:

Page 4.

The main medium and long term funding provided by banks are in the form of Project Finance. Project finance is the process of financing a specific economic unit that the sponsors create, in which creditors share much of the venture’s business risk and funding is obtained strictly for the project itself. Therefore, the correct option is B.

The main medium and long term funding provided by banks are in the form of Project Finance. Project finance is the process of financing a specific economic unit that the sponsors create, in which creditors share much of the venture’s business risk and funding is obtained strictly for the project itself. Therefore, the correct option is B.

Soru 58

Which of the followings is not among the possible costs considering long-term loans?

Seçenekler

A

Covenant compliance fees.

B

Arrangement fees.

C

Lease.

D

Professional advice.

E

Interest.

Açıklama:

Page 4.

Project finance transactions are complex undertakings, they have higher costs of borrowing when compared to conventional financing and the negotiation of the financing and operating agreements is time-consuming. The costs applicable loans can be in the forms of:

• interest

• arrangement fees

• covenant compliance costs

• professional advice.

Therefore, the correct option is C.

Project finance transactions are complex undertakings, they have higher costs of borrowing when compared to conventional financing and the negotiation of the financing and operating agreements is time-consuming. The costs applicable loans can be in the forms of:

• interest

• arrangement fees

• covenant compliance costs

• professional advice.

Therefore, the correct option is C.

Soru 59

Which of thefollowings is the type of loan which multple banks agree upon and undertake?

Seçenekler

A

Project finance.

B

Syndication loans.

C

Mortgage.

D

Bank overdraft.

E

Revolving credits.

Açıklama:

Page 5.

Syndication loans are credits granted by a group of banks to a borrower. In a syndication loan, two or more banks agree jointly to make a loan to a borrower. Every syndicate member has a separate claim on the debtor, although there is a single loan agreement contract. Therefore, the correct option is B.

Syndication loans are credits granted by a group of banks to a borrower. In a syndication loan, two or more banks agree jointly to make a loan to a borrower. Every syndicate member has a separate claim on the debtor, although there is a single loan agreement contract. Therefore, the correct option is B.

Soru 60

When debt and equity are considered, which of the followings is correct?

Seçenekler

A

Unpaid debt is a liability of the firm.

B

Debt is an ownership interest in the firm.

C

Creditors generally have voting power over debt.

D

Creditors cannot legally claim the assets of the firm over unpaid debt.

E

Interest on debt is not tax deductible.

Açıklama:

Page 6.

The main differences between debt and equity are the following:

• Debt is not an ownership interest in the firm. Creditors do not generally have voting power.

• The corporation’s payment of interest on debt is considered a cost of doing business and is fully tax deductible. Dividends paid to stockholders are not tax deductible.

• Unpaid debt is a liability of the firm. If it is not paid, the creditors can legally claim the assets of the firm. This action can result in liquidation or reorganization, two of the possible consequences of bankruptcy. Thus, one of the costs of issuing debt is the possibility of financial failure. This possibility does not arise when equity is issued.

Therefore, the correct option is A.

The main differences between debt and equity are the following:

• Debt is not an ownership interest in the firm. Creditors do not generally have voting power.

• The corporation’s payment of interest on debt is considered a cost of doing business and is fully tax deductible. Dividends paid to stockholders are not tax deductible.

• Unpaid debt is a liability of the firm. If it is not paid, the creditors can legally claim the assets of the firm. This action can result in liquidation or reorganization, two of the possible consequences of bankruptcy. Thus, one of the costs of issuing debt is the possibility of financial failure. This possibility does not arise when equity is issued.

Therefore, the correct option is A.

Ünite 2

Soru 1

What is the average cost of the mix of debt and equity?

Seçenekler

A

Cost of capital

B

Cost of debt

C

Cost of equity

D

Cost of common equity

E

Mrginal cost of capital

Açıklama:

Every business requires capital to invest. Therefore, capital is the most important factor of production and the cost of capital is the most significant determinant in investment decisions. The cost of capital is the average cost of the capital mix (the mix of debt and equity in financing decisions). The correct answer is A.

Soru 2

What is the weighted average cost of capital?

Seçenekler

A

The average cost of the capital mix

B

The weight of the debt component

C

The average cost of the different types of capital

D

The weight of the equity component

E

The return a company requires to decide

Açıklama:

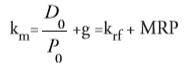

Normally, a business follows a target capital structure, where the percentages of different financing sources are set in an effort to minimize the average cost of capital. The weighted average cost of capital (WACC) is the average cost of the different types of capital employed by the firm. The correct answer is C.

Soru 3

Which of the following equations is used to measure WACC?

Seçenekler

A

B

C

D

E

Açıklama:

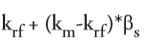

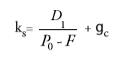

The weighted average cost of capital (WACC) is the average cost of the different types of capital employed by the firm and is measured with the equation below:

where wD is the weight of the debt component and wCE is the weight of the equity component. T is the tax rate and after-tax cost of debt component is calculated by multiplying the before-tax cost of debt (kD) by the tax deductibility. Cost of equity component is denoted as kCE in the above equation. The correct answer is B.

Soru 4

What is the benchmark rate that represents the interest rate at which banks offer to lend funds to one another in the international interbank market for short-term loans?

Seçenekler

A

Bond yield

B

Risk premium

C

Common equity

D

LIBOR

E

Risk free rate

Açıklama:

Banks borrow from international bank loans at floating rates and the index is almost always the LIBOR (London Interbank Offered Rate). LIBOR is a benchmark rate that represents the interest rate at which banks offer to lend funds to one another in the international interbank market for short-term loans. LIBOR is an average value of the interestrate which is calculated from estimates submitted by the leading global banks on a daily basis. The correct answer is D.

Soru 5

In which of the following is the interest rate floating and not fixed?

Seçenekler

A

Callable bonds

B

Convertible bonds

C

Preferred bonds

D

Bonds with sinking funds

E

Indexed bonds

Açıklama:

In bond issues, if the interest rate is floating and not fixed, then it is called as an indexed bond. The index can be any economic indicator but mostly it is a price index, such as the inflation rate, the oil price or the gold price index. The correct answer is E.

Soru 6

- They are issued without a maturity.

- The stockholder receives floating dividends that are deductible.

- In some ways, they resemble to bonds, in others to common stocks.

- Preferred dividends are paid out before the dividends to common stockholders.

Seçenekler

A

I and II

B

III and IV

C

I, II and III

D

I, III and IV

E

II, III and IV

Açıklama:

Preferred stocks;

- are issued without a maturity (I),

- resemble to bonds in some ways, in others to common stocks (III),

- require preferred dividends to be paid out before the dividends to common stockholders (IV).

Soru 7

XLM Corp. has a bond issue outstanding for which the yield-to-maturity is 8.45%. Analysts estimate a risk premium of 3.15% for the company's stock. What is the expected cost of equity of XLM according to the bond-yield-plus-risk-premium approach?

Seçenekler

A

05.53%

B

10.30%

C

11.60%

D

12.45%

E

14.90%

Açıklama:

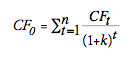

The bond-yield-plus-risk-premium approach provides a practical but highly subjective solution to the estimation of the cost of equity. The approach is based upon adding up a risk premium over the firm’s bond yield. Thus, the cost of equity is calculated straightforward by the following simple computation:

k= 0.0845 + 0.0315= 0.1160

k= 0.0845 + 0.0315= 0.1160

According to the bond-yield-plus-risk-premium approach, XLM’s expected cost of equity is 11.60%. The correct answer is C.

According to the bond-yield-plus-risk-premium approach, XLM’s expected cost of equity is 11.60%. The correct answer is C.

Soru 8

Which of the following equations is used to adjust the cost of equity to flotation costs?

Seçenekler

A

B

C

D

E

Açıklama:

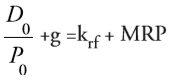

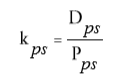

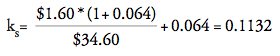

Firms may also raise external equity capital by issuing new shares. In this case, the firm will have to incur some flotation (transaction) costs which will eventually raise the cost of equity. In order to adjust the cost of equity to flotation costs, we use the following equation:

where F shows the flotation costs incurred during the issue of the new shares. By incorporating the flotation costs in the model, the rise in the cost of equity after new stock offerings is accounted for. The correct answer is B.

where F shows the flotation costs incurred during the issue of the new shares. By incorporating the flotation costs in the model, the rise in the cost of equity after new stock offerings is accounted for. The correct answer is B.Soru 9

A & B Corp. has the following optimal capital structure:

- Long-term Debt 20%

- Preferred Stocks 10%

- Common Equity 40%

Seçenekler

A

4.24%

B

4.60%

C

5.46%

D

6.30%

E

8.14%

Açıklama:

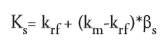

The cost of each capital component is weighed at the proportions in the capital structure to quantify the firm’s WACC.

, where wD is the weight of debt financing in the capital structure, kD is the cost component of debt funds, T is the tax rate, accordingly wPS is the weight of preferred stocks, kPS is its cost component, wCE is the weight of common equity and kCE is the cost of equity capital. Therefore;

, where wD is the weight of debt financing in the capital structure, kD is the cost component of debt funds, T is the tax rate, accordingly wPS is the weight of preferred stocks, kPS is its cost component, wCE is the weight of common equity and kCE is the cost of equity capital. Therefore;

WACC=0.20*0.07*(1-0.40)+0.10*0.13+0.40*0.15=0.0814

As it can be seen from the above calculation the WACC for A & B is 8.14%. The correct answer is E.

WACC=0.20*0.07*(1-0.40)+0.10*0.13+0.40*0.15=0.0814

As it can be seen from the above calculation the WACC for A & B is 8.14%. The correct answer is E.

Soru 10

NEO Corp. has the following optimal capital structure:

- Long-term Debt 40%

- Preferred Stocks 30%

- Common Equity 60%

Seçenekler

A

15.80%

B

16.40%

C

18.50%

D

20.60%

E

22.70%

Açıklama:

The cost of each capital component is weighed at the proportions in the capital structure to quantify the firm’s WACC.

, where wD is the weight of debt financing in the capital structure, kD is the cost component of debt funds, T is the tax rate, accordingly wPS is the weight of preferred stocks, kPS is its cost component, wCE is the weight of common equity and kCE is the cost of equity capital. Therefore;

WACC=0.40*0.10*(1-0.35)+0.30*0.20+0.60*0.12=0.1580

As it can be seen from the above calculation the WACC for A & B is 15.80%. The correct answer is A.

WACC=0.40*0.10*(1-0.35)+0.30*0.20+0.60*0.12=0.1580

As it can be seen from the above calculation the WACC for A & B is 15.80%. The correct answer is A.

Soru 11

Which of the following is a benchmark rate that represents the interest rate at which banks offer to lend funds to one another in the international interbank market for short-term loans?

Seçenekler

A

LIBOR

B

Convertible bond

C

Floating rates

D

Risk premium

E

Option

Açıklama:

LIBOR is a benchmark rate that represents the interest rate at which banks offer to lend funds to one another in the international interbank market for short-term loans.

Soru 12

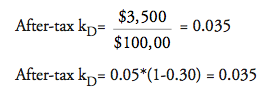

XYZ Corp. borrows $200,000 as a bank loan at an annual interest rate of 10%. The company pays 25% corporate tax rate. What is the after-tax rate of borrowing for XYZ Corp.?

Seçenekler

A

0.025

B

0.05

C

0.075

D

0.1

E

0.15

Açıklama:

After-tax kD=kD*(1-T)

After-tax kD=0.10*(1-0.25)= 0.075

After-tax kD=0.10*(1-0.25)= 0.075

Soru 13

BB Corp. borrows $50,000 as a bank loan at an annual interest rate of 5%. The company pays 20% corporate tax rate. What is the after-tax rate of borrowing for BB Corp.?

Seçenekler

A

0.04

B

0.05

C

0.06

D

0.075

E

0.08

Açıklama: