Audıtıng (ENG) - Tüm Sorular

Ünite 1

Soru 1

Which of the following is definition of information risk?

Seçenekler

A

Information risk reflects the possibility of making mistakes in decisions to be taken regarding the business.

B

Information risk reflects the possibility of not to measure the success of using economic resources.

C

Information risk reflects the conflict of interest between the users of the financial statements and the company managers responsible for the preparation of the financial statements.

D

Information risk means increases in the number of information users.

E

Information risk reflects the need for accurate and reliable information.

Açıklama:

Information risk reflects the possibility of making mistakes in decisions to be taken regarding the business.

Soru 2

All of the following will cause to information risk except:

Seçenekler

A

Interest of regulatory institutions

B

Being far from the information

C

Bias of the information provider

D

Large volume data

E

Complex accounting operations

Açıklama:

Causes of information risk:

• Being far from the information

• Bias of the information provider

• Large volume data

• Complex accounting operations

• Being far from the information

• Bias of the information provider

• Large volume data

• Complex accounting operations

Soru 3

The financial statements of the enterprises should be subject to independent audit by independent auditors for some reasons. One of the reason is "Conflict of Interest". Which of the following parties has a conflict of interest?

Seçenekler

A

There may be conflict of interest between the users of the financial statements and the company managers

responsible for the preparation of the financial statements.

responsible for the preparation of the financial statements.

B

There may be conflict of interest between the internal auditors and the company managers responsible for the preparation of the financial statements.

C

There may be conflict of interest between the internal auditors and external auditors.

D

There may be conflict of interest between the users of the financial statements and the internal auditors

E

There may be conflict of interest between the users of the financial statements and the regulators.

Açıklama:

There may be conflict of interest between the users of the financial statements and the company managers

responsible for the preparation of the financial statements.

responsible for the preparation of the financial statements.

Soru 4

All of the followings are benefits of independent audit except:

Seçenekler

A

Helps the management to increase their wealth with the scarce resources they have.

B

Helps the management to make predictions and analyses regarding the financial statements and to

make healthy future decisions.

make healthy future decisions.

C

Indicates whether the financial statements reflect the truth.

D

Helps business management and employees to prevent cheating.

E

Provides correct flow of information to management.

Açıklama:

The benefits of independent audit can be listed as follows;

1. Provides correct flow of information to management.

2. Helps the management to make predictions and analyses regarding the financial statements and to

make healthy future decisions.

3. Indicates whether the financial statements

reflect the truth.

4. Helps business management and employees

to prevent cheating.

1. Provides correct flow of information to management.

2. Helps the management to make predictions and analyses regarding the financial statements and to

make healthy future decisions.

3. Indicates whether the financial statements

reflect the truth.

4. Helps business management and employees

to prevent cheating.

Soru 5

Which of the following differs between Control and Audit?

Seçenekler

A

Control is the beginning of the audit or the activity that precedes the audit.

B

Control is the examination to find out the truth of something or whether things are being carried out well.

C

Control can be defined as an examination to find out the truth of something.

D

Control is to review, to examine again. It is mostly the examination of financial events and tax accounts.

E

Auditing is mostly used for the re-examination and control of financial events.

Açıklama:

The concept of audit is confused with various concepts such as Control, Inspection and Revision.

Before defining the concept of audit, let’s define the concepts that lead to this confusion.

“Control is the beginning of the audit or the activity that precedes the audit. The measures taken to

achieve the objectives are a control activity.” Certain measures are taken to make sure that something turns

out as desired or to achieve a certain goal.

Before defining the concept of audit, let’s define the concepts that lead to this confusion.

“Control is the beginning of the audit or the activity that precedes the audit. The measures taken to

achieve the objectives are a control activity.” Certain measures are taken to make sure that something turns

out as desired or to achieve a certain goal.

Soru 6

Which of the following is one of the major concepts as a subject of independent audit in Independent Audit definition?

Seçenekler

A

The subject of independent audit is financial statements and footnotes prepared by the company.

B

The subject of independent audit is Generally Accepted Accounting Principles and Concepts (GAAP)

C

The subject of independent audit is Turkey Accounting Standards (TAS).

D

The subject of independent audit is The Generally Accepted Auditing Standards (GAAS).

E

The subject of independent audit is Generellay Accepted Accounting Principles and International Financial

Reporting Standards (IFRS)

Reporting Standards (IFRS)

Açıklama:

Important concepts in the definition of independent audit are shown in Figure 1.4;

The subject of independent audit is financial statements and footnotes prepared by the company.

The subject of independent audit is financial statements and footnotes prepared by the company.

Soru 7

According to the independent audit definition the independent audit is based on predetermined criteria. Which of the following is the major predetermined criteria which the auditors will evaluate the information?

Seçenekler

A

Generally Accepted Accounting Principles and Concepts (GAAP) and Turkey Accounting Standards (TAS)

B

The Generally Accepted Auditing Standards (GAAS)

C

The Generally Accepted Turkish Auditing Standards (GATAS)

D

Turkish Auditing Standards (TAS)

E

American Accounting Association (AAA)

Açıklama:

There are three important elements to be noted

in this definition. The first of these is that the

independent audit is based on predetermined

criteria. These criteria are Generally Accepted

Accounting Principles and Concepts (GAAP) and

Turkey Accounting Standards (TAS), according to

which the auditors will evaluate the information.

in this definition. The first of these is that the

independent audit is based on predetermined

criteria. These criteria are Generally Accepted

Accounting Principles and Concepts (GAAP) and

Turkey Accounting Standards (TAS), according to

which the auditors will evaluate the information.

Soru 8

Which of the followings are types of Audit by Reason?

Seçenekler

A

compulsory audit and optional audit

B

Independent audit and financial statement audit

C

compliance audit and internal audit.

D

Compliance Audit and Public Audit

E

Performance Audit and Operational Audit

Açıklama:

a. Types of Audit by Reason

The types of audit are divided into two according

to the reasons for their execution; compulsory

audit and optional audit.

The types of audit are divided into two according

to the reasons for their execution; compulsory

audit and optional audit.

Soru 9

Compulsory Audit is also known as ....

Seçenekler

A

Legal Audit

B

Optional Audit

C

Supervisory Audit

D

Compliance Audit

E

Public Sector Audit

Açıklama:

Compulsory Audit is also known as Legal Audit

Soru 10

Which of the following auditors are the auditors who are included in the organization chart of the

organization they are affiliated with and operate directly under the board of directors or under the general

manager?

organization they are affiliated with and operate directly under the board of directors or under the general

manager?

Seçenekler

A

Internal auditors

B

Public auditors

C

Public Sector Auditors

D

External auditors

E

Independent auditors

Açıklama:

Internal auditors Internal auditors are the auditors who are included in the organization chart of the

organization they are affiliated with and operate directly under the board of directors or under the general

manager.

organization they are affiliated with and operate directly under the board of directors or under the general

manager.

Soru 11

When was the term audit first used?

Seçenekler

A

1265

B

1270

C

1278

D

1284

E

1289

Açıklama:

The term auditor was first used in 1289.

Soru 12

Which of the following trues about the “Systems Based Audit Approach”?

Seçenekler

A

It was used for the examination of all documents before and after the industrial revolution.

B

It was used in the period of in the period of 1900-1930.

C

It is based on the examination of the internal control structure of the enterprises.

D

It is a result of the widespread use of activity audit as a result of today’s developments in information technology and audit field.

E

It appeared after large-scale financial scandals encountered after the 2000s.

Açıklama:

The “Systems Based Audit Approach”, which has come from the 1930s until today and is based on the examination of the internal control structure of the enterprises.

Soru 13

Which of the following are among information risks?

I. Being far from the information

II. Bias of the information providers

III. Large volume data

IV. Complex accounting operations

I. Being far from the information

II. Bias of the information providers

III. Large volume data

IV. Complex accounting operations

Seçenekler

A

I & II

B

I, II & IV

C

II & III

D

III & IV

E

I, II, III & IV

Açıklama:

Causes of information risk are:

- Being far from the information

- Bias of the information provider

- Large volume data

- Complex accounting operations

Soru 14

Which of the following is a internal information user?

Seçenekler

A

Shareholders

B

Investors

C

Creditors

D

Government

E

Customers

Açıklama:

Owners, Shareholders, Management, & Employees are internal information users.

Soru 15

Which of the following is an external information user?

Seçenekler

A

Owners

B

Suppliers

C

Shareholders

D

Management

E

Employees

Açıklama:

Investors, Creditors, Government, Customers & Suppliers are external information users.

Soru 16

___________ Audit is an audit made by companies or organizations of their own accord without any legal obligation.

Seçenekler

A

Compulsory

B

Legal

C

Internal

D

Optional

E

Compliance

Açıklama:

Optional (Supervisory Audit): It is an audit made by companies or organizations of their own accord without any legal obligation.

Soru 17

Another name for Internal Audit is ……… Audit.

Seçenekler

A

Supervisory

B

Performance

C

Financial Satetement

D

Legal

E

Independent

Açıklama:

Another name for Internal Audit is Performance Audit or Operational Audit.

Soru 18

The purpose of ________ audit is to evaluate the efficiency and effectiveness of the activities of the enterprises.

Seçenekler

A

Supervisory

B

Compliance

C

Financial Statement

D

Internal

E

Optional

Açıklama:

The purpose of internal audit is to evaluate the efficiency and effectiveness of the activities of the enterprises.

Soru 19

___________ audit is carried out in order to determine whether the activities or transactions of the enterprises comply with.

Seçenekler

A

Public

B

Financial Statement

C

Optional

D

Independent

E

Compulsory

Açıklama:

Public Audir or Compliance audit is carried out in order to determine whether the activities or transactions of the enterprises comply with certain methods and rules and the relevant legislation. In compliance audit, it is checked whether the rules determined by an authority are complied with.

Soru 20

Which of the following are among different types of auditors?

I. Private Auditor

II. Independent (External) Auditors

III. Internal Auditors

IV. Public Sector Auditors

I. Private Auditor

II. Independent (External) Auditors

III. Internal Auditors

IV. Public Sector Auditors

Seçenekler

A

I, II & III

B

Only I

C

Only I & IV

D

II, III & IV

E

Only III & IV

Açıklama:

There are three types of auditors:

- Independent (External) Auditors

- Internal Auditors

- Public Sector Auditors

Ünite 2

Soru 1

Which of the following institution is authorized in the development and publication of auditing standards, quality control standards and code of ethics in Turkey?

Seçenekler

A

KGK (Public Oversight, Accounting and Auditing Standards Authority)

B

IFAC (International Federation of Accountants)

C

IAASB (The International Auditing and Assurance Standards Board)

D

AICPA (American Institute of Certified Public Accountants

E

CMB (Capital Market Board)

Açıklama:

If we examine the institutions that are

authorized in the development and publication

of auditing standards, quality control standards

and code of ethics in Turkey and in the World;

IFAC (International Federation of Accountants) is

authorized in the world, KGK (Public Oversight,

Accounting and Auditing Standards Authority) is

authorized in Turkey.

authorized in the development and publication

of auditing standards, quality control standards

and code of ethics in Turkey and in the World;

IFAC (International Federation of Accountants) is

authorized in the world, KGK (Public Oversight,

Accounting and Auditing Standards Authority) is

authorized in Turkey.

Soru 2

IFAC’s strategic actions are grouped under three strategic objectives which are .....

Seçenekler

A

integrity, expertise, transparency

B

Relevance, Usefulness, The best evidence

C

Testimonial, Documentary, Analytical

D

Thorough, Complete, Relevante

E

Complete, precise, accurate.

Açıklama:

IFAC’s member organizations serve the public

interest by enhancing the relevance, reputation, and

value of the global accountancy profession. IFAC’s

strategic actions are grouped under three strategic

objectives (integrity, expertise, transp

IFAC’s strategic actions are grouped under three strategic

objectives (integrity, expertise, transparency) and

leverage IFAC’s unique position.

interest by enhancing the relevance, reputation, and

value of the global accountancy profession. IFAC’s

strategic actions are grouped under three strategic

objectives (integrity, expertise, transp

IFAC’s strategic actions are grouped under three strategic

objectives (integrity, expertise, transparency) and

leverage IFAC’s unique position.

Soru 3

How can the work of the international, independent standard-setting boards support the global economy and

financial markets?

financial markets?

Seçenekler

A

by producing high-quality, global standards for audit and assurance, professional ethics, public sector financial reporting, and professional skills and competencies.

B

by providing objectives, standards, and an evaluation-reward system.

C

by appraising the effectiveness and efficiency of operations and programs.

D

by notifying governmental regulatory agencies of unethical business practices by organization management

E

by reviewing the compliance with laws, regulations, policies, procedures, and contracts

Açıklama:

The work of the international, independent standard-setting boards supports the global economy and

financial markets by producing high-quality, global standards for audit and assurance, professional ethics,

public sector financial reporting, and professional skills and competencies.

financial markets by producing high-quality, global standards for audit and assurance, professional ethics,

public sector financial reporting, and professional skills and competencies.

Soru 4

In order to ensure that the audit is more qualified in Turkey, which institution has the KGK signed a copyright agreement in 2013?

Seçenekler

A

International Federation of Accountants (IFAC)

B

The International Public Sector Accounting Standards Board (IPSASB)

C

International Standards on Related Services (ISR)

D

Institute of Certified Public Accountants (AICPA)

E

Generally accepted auditing standards Board (GAAS)

Açıklama:

In order to ensure audit to be qualified in Turkey, the KGK signed a copyright agreement

with International Federation of Accountants (IFAC) in 2013.

with International Federation of Accountants (IFAC) in 2013.

Soru 5

Which of the following is the measure of the quality of the auditor’s audit performance?

Seçenekler

A

Auditing standards

B

Code of Ethics

C

Quality Control devices

D

Assurance and Related Services Engagements

E

Analytical Procedures

Açıklama:

Auditing standards are the measure of the quality of the auditor’s audit performance.

Soru 6

Which of the following set of systematic guidelines will be used by auditors when conducting audits on companies’ financial records?

Seçenekler

A

Generally accepted auditing standards

B

Generally Accepted Accounting Standards

C

Generally Accepted Accounting Principles

D

Audit Sampling

E

Accounting Estimates

Açıklama:

Generally accepted auditing standards (GAAS) are a set of systematic guidelines used by auditors when

conducting audits on companies’ financial records.

conducting audits on companies’ financial records.

Soru 7

Which of the following standards address the important qualifications of the auditor should possess?

Seçenekler

A

General standards

B

Standards of Field Work

C

The Standards of Reporting

D

The Standards of Circumstances

E

The Standards of quality

Açıklama:

General standards address the important qualifications of the auditor should possess.

Soru 8

Which type of opinion will be expressed by the auditor when the auditor concludes that the financial statements are prepared fairly, in all material respects, in accordance with the applicable financial reporting framework and conformity and accordance with generally accepted accounting principles (GAAP)?

Seçenekler

A

Unmodified opinion

B

Qualified Opinion

C

Unqualified Opinion

D

Modified opinion

E

Fair opinion

Açıklama:

Unmodified opinion : T

The opinion expressed by the auditor when the auditor concludes that

the financial statements are prepared fairly, in all

material respects, in accordance with the applicable

financial reporting framework and conformity and

accordance with generally accepted accounting principles (GAAP)

Unmodified opinion :

The opinion expressed by the auditor when the auditor concludes that

the financial statements are prepared fairly, in all

material respects, in accordance with the applicable

financial reporting framework and conformity and

accordance with generally accepted accounting principles (GAAP)

The opinion expressed by the auditor when the auditor concludes that

the financial statements are prepared fairly, in all

material respects, in accordance with the applicable

financial reporting framework and conformity and

accordance with generally accepted accounting principles (GAAP)

Unmodified opinion :

The opinion expressed by the auditor when the auditor concludes that

the financial statements are prepared fairly, in all

material respects, in accordance with the applicable

financial reporting framework and conformity and

accordance with generally accepted accounting principles (GAAP)

Soru 9

A professional accountant shall comply with each of the fundamental principles. The fundamental

principles of ethics establish the standard of behavior expected of a professional accountant. Which of the following is NOT one of these fundamental principles?

principles of ethics establish the standard of behavior expected of a professional accountant. Which of the following is NOT one of these fundamental principles?

Seçenekler

A

Accuracy

B

Integrity

C

Objectivity

D

Professional Competence and Due Care

E

Confidentiality

Açıklama:

The Fundamental Principles

A professional accountant shall comply with each of the fundamental principles. The fundamental

principles of ethics establish the standard of behavior expected of a professional accountant. These

fundamental principles are:

• Integrity

• Objectivity

• Professional Competence and Due Care

• Confidentiality

• Professional Behavior

A professional accountant shall comply with each of the fundamental principles. The fundamental

principles of ethics establish the standard of behavior expected of a professional accountant. These

fundamental principles are:

• Integrity

• Objectivity

• Professional Competence and Due Care

• Confidentiality

• Professional Behavior

Soru 10

One of the fundamental principles of ethics is "Integrity". Professional accountants must be ..... and ..... during their work in all professional and business relationships at all times.

Seçenekler

A

honest and straightforward

B

objective and accurate

C

careful and precise

D

competent and comply with

E

Confident and professional

Açıklama:

Integrity: Professional accountants must be

honest and straightforward during their work

in all professional and business relationships at

all times.

honest and straightforward during their work

in all professional and business relationships at

all times.

Soru 11

Auditing standards provide a ................ and the objectives to be achieved in an audit

Seçenekler

A

measure of audit quality

B

aim

C

goal

D

assurance

E

principal

Açıklama:

Auditing standards provide a measure of audit quality and the objectives to be achieved in an audit.

Soru 12

.......... is the global organization for the accountancy profession, comprising more than 175 member and associate organizations in 130 countries and jurisdictions, representing nearly 3 million professional accountants.

Seçenekler

A

IFAC

B

IACC

C

ICAAN

D

FAIC

E

FAAC

Açıklama:

IFAC is the global organization for the accountancy profession, comprising more than 175 member and associate organizations in 130 countries and jurisdictions, representing nearly 3 million professional accountants.

Soru 13

The ........ is responsible for achieving an effective public oversight in Turkey. The ........ is also responsible for setting standards that ensure the preparation and auditing of financial statements in compliance with international standards.

Seçenekler

A

KGK

B

ISR

C

IAESB

D

IESBA

E

IPSASB

Açıklama:

The KGK is responsible for achieving an effective public oversight in Turkey. The KGK is also responsible for setting standards that ensure the preparation and auditing of financial statements in compliance with international standards.

Soru 14

.............. develops standards, guidance, and resources for use by public sector entities around the world for preparation of general purpose financial statements.

Seçenekler

A

The International Public Sector Accounting Standards Board

B

The International Ethics Standards Board for Accountants

C

The International Accounting Education Standards Board

D

InternationalStandardsonRelatedServices

E

International Standards on Assurance Engagement

Açıklama:

The International Public Sector Accounting Standards Board develops standards, guidance, and resources for use by public sector entities around the world for preparation of general purpose financial statements.

Soru 15

Which of the followings is responsible for approving generally accepted auditing standards?

Seçenekler

A

AICPA

B

GAAS

C

ISAE

D

ISRS

E

TSRS

Açıklama:

Generally accepted auditing standards have been approved and adopted by the membership of the AICPA

Soru 16

Which of the followings is a standard for reporting in audit?

Seçenekler

A

Adequacy of Onformative Disclosures

B

Adequate Technical Training and Proficiency

C

Understand the Client’s Internal Control

D

Address the qualifications of the auditor and the quality of his/her work

E

Address the planning and performing audit

Açıklama:

Adequacy of Onformative Disclosures is described as reporting standard in Generally Accepted Auditing Standards

Soru 17

The auditor’s responsibility is to form an opinion on the financial statements. Which of the following is related to GAAP standards on reporting?

Seçenekler

A

Expression of Opinion on Financial Statements

B

Circumstances When GAAP not Consistently Followed

C

Whether Statements were Prepared in Accordance With GAAP

D

Adequacy of Informative Disclosures

E

Understand the Client’s Internal Control

Açıklama:

The auditor’s responsibility is to form an opinion on the financial statements. Auditor’s report indicates the degree of the responsibilities. The auditor’s report shall be in writing. The auditor’s opinion varies according to the importance of the violation in the reporting standards and its impact on the financial statement. This called Expression of Opinion on Financial Statements in GAAP

Soru 18

Professional accountants must be honest and straightforward during their work in all professional and business relationships at all times. What is the name of this ethic standard?

Seçenekler

A

Integrity

B

Objectivity

C

Professional Competence and Due Care

D

Confidentiality

E

Professional Behavior

Açıklama:

Professional accountants must be honest and straightforward during their work in all professional and business relationships at all times. This is called integrity in GAAP

Soru 19

Which of the following definitions belong to Objectivity ethic standards in accounting?

Seçenekler

A

Not to compromise professional or business judgment because of bias, conflict of interest or undue influence of others.

B

Be honest and straightforward during their work in all professional and business relationships at all times.

C

Be up to date with technical, professional and business developments.

D

Respect the confidentiality of information acquired as a result of professional and business relationships.

E

Comply with relevant laws and regulations and avoid all actions the accountant knows or should know might discredit the profession.

Açıklama:

A professional accountant shall comply with the principle of objectivity, which requires an accountant not to compromise professional or business judgment because of bias, conflict of interest or undue influence of others.

Soru 20

Which of the followings is related to monitoring in audit?

Seçenekler

A

Designing a process to provide it with reasonable assurance that the policies and procedures relating to the system of quality control are relevant, adequate, and operating effectively.

B

Establishing policies and procedures designed to promote an internal culture recognizing that quality is essential in performing engagements.

C

Establishing policies and procedures designed to provide it with reasonable assurance that the firm and its personnel comply with relevant ethical requirements.

D

Establishing policies and procedures for the acceptance and continuance of client relationships and specific engagements.

E

Establishing policies and procedures designed to provide it with reasonable assurance that engagements are performed in accordance with professional standards and legal and regulatory requirements.

Açıklama:

The firm shall establish a monitoring process designed to provide it with reasonable assurance that the policies and procedures relating to the system of quality control are relevant, adequate, and operating effectively. Policies and procedures related with monitoring are ensuring harmony with professional standards and legal and regulatory requirements and the system of quality control has been appropriately designed and effectively implemented.

Ünite 3

Soru 1

Which ethical requirement is violated by the audit firm if information is disclosed to third parties without proper and specific authority?

Seçenekler

A

Integrity

B

Objectivity

C

Confidentiality

D

Independence

E

Professional behaviour

Açıklama:

Confidentiality is the ethical requirement explained in the question.

To respect the confidentiality of information acquired as a result of professional and business relationships, and therefore, not disclose

any such information to third parties without proper and specific authority, unless there is a legal or professional right or duty to disclose, nor use the information for his/her personal advantage or for the

advantage of third parties.

To respect the confidentiality of information acquired as a result of professional and business relationships, and therefore, not disclose

any such information to third parties without proper and specific authority, unless there is a legal or professional right or duty to disclose, nor use the information for his/her personal advantage or for the

advantage of third parties.

Soru 2

If the auditor’s father is the chief executive officer of the client firm, which ethical requirement is violated?

Seçenekler

A

Independence

B

Integrity

C

Objectivity

D

Confidentiality

E

Professional behaviour

Açıklama:

This is an example of a breach of independence due to family and personal relationship between the auditor and the chief executive officer.

This is related to independence.

This is related to independence.

Soru 3

Which of the following is not one of the policies and procedures of human resources in audit firms?

Seçenekler

A

Recruitment

B

Performance evaluation

C

Promotion

D

Acceptance

E

Career development

Açıklama:

Some of policies and procedures of human

resources in audit firms should include the

following items (ISQC 1.A24):

• Recruitment

• Performance evaluation

• Capabilities

• Competence

• Career development

• Promotion

• Compensation

• The estimation of personnel needs

Acceptance is not related to human resources but it is before that step.

resources in audit firms should include the

following items (ISQC 1.A24):

• Recruitment

• Performance evaluation

• Capabilities

• Competence

• Career development

• Promotion

• Compensation

• The estimation of personnel needs

Acceptance is not related to human resources but it is before that step.

Soru 4

"Work is assigned to staff who have adequate technical training and proficiency."

Which human resource procedure expected from the firm is explained in the following sentence?

Which human resource procedure expected from the firm is explained in the following sentence?

Seçenekler

A

Recruitment

B

Competence

C

Career development

D

Promotion

E

Compensation

Açıklama:

Work is assigned to staff who have

adequate technical training and proficiency

(competence).

The sentence is related to competence.

adequate technical training and proficiency

(competence).

The sentence is related to competence.

Soru 5

"Examples of the ------------------ process include ongoing evaluation

of the audit firm’s system of internal control, annual testing of quality control procedures and periodic inspection of at least one completed engagement."

Which of the following terms could best complete the blank in the sentence above?

of the audit firm’s system of internal control, annual testing of quality control procedures and periodic inspection of at least one completed engagement."

Which of the following terms could best complete the blank in the sentence above?

Seçenekler

A

Monitoring

B

Engagement

C

Human Resources

D

Documentation

E

Acceptance

Açıklama:

Examples of the monitoring process include ongoing evaluation

of the audit firm’s system of internal control, annual testing of quality control procedures and periodic inspection of at least one completed engagement.

Monitoring is the correct answer.

of the audit firm’s system of internal control, annual testing of quality control procedures and periodic inspection of at least one completed engagement.

Monitoring is the correct answer.

Soru 6

Which of the following audit risk types generate from the client firm and the auditor has no effect on it?

Seçenekler

A

Detection risk

B

Business risk

C

Sampling risk

D

Non-sampling risk

E

Risk of material misstatement

Açıklama:

Risk of material misstatement is the risk that financial statements are materially misstated prior to audit (ISA 200.13n). It is generated from the client firm. The auditor has no effect on it.

The risk whose responsibility lies on the firm not the auditor is risk of material misstatement.

The risk whose responsibility lies on the firm not the auditor is risk of material misstatement.

Soru 7

-It is the risk resulting from significant conditions, events,

circumstances, actions and inactions that could adversely affect an entity’s ability to achieve its objectives and execute its

strategies.

-It is a risk generated from setting of inappropriate objectives and strategies.

Which type of audit risk is explained above?

circumstances, actions and inactions that could adversely affect an entity’s ability to achieve its objectives and execute its

strategies.

-It is a risk generated from setting of inappropriate objectives and strategies.

Which type of audit risk is explained above?

Seçenekler

A

Inherent risk

B

Control risk

C

Account risk

D

Business risk

E

Detection risk

Açıklama:

Business risk: It is the risk resulting

from significant conditions, events,

circumstances, actions and inactions that

could adversely affect an entity’s ability

to achieve its objectives and execute its

strategies. It is a risk generated from setting

of inappropriate objectives and strategies

(ISA 315.4b). For example, businesses in

the electronics industry experience high

business risk leading to high inherent

risk for inventory obsolescence due to

technological developments

The answer is business risk.

from significant conditions, events,

circumstances, actions and inactions that

could adversely affect an entity’s ability

to achieve its objectives and execute its

strategies. It is a risk generated from setting

of inappropriate objectives and strategies

(ISA 315.4b). For example, businesses in

the electronics industry experience high

business risk leading to high inherent

risk for inventory obsolescence due to

technological developments

The answer is business risk.

Soru 8

Which management assertion is exemplified in the following sentence?

"All required disclosures related to bankloans are included in the financial statement footnotes."

"All required disclosures related to bankloans are included in the financial statement footnotes."

Seçenekler

A

Accuracy

B

Completeness

C

Valuation

D

Classification

E

Occurence

Açıklama:

"All existing inventory has been counted and

included in the inventory summary." is an example of completeness as a management assertion.

Completeness: The auditor will check whether all amounts that should be included have actually been included.

included in the inventory summary." is an example of completeness as a management assertion.

Completeness: The auditor will check whether all amounts that should be included have actually been included.

Soru 9

Which of the following is the reason why the auditor

cannot guarantee 100% correctness of financial statements?

cannot guarantee 100% correctness of financial statements?

Seçenekler

A

because the auditor obtains audit evidence on whether the financial statements are prepared in compliance with the applicable financial reporting framework.

B

because the auditor is supposed to declare that he/she performed all audit process in line with auditing standards and applicable legal framework.

C

because the audit opinion is based on the audit evidence obtained through audit sampling.

D

because the auditor is responsible for preparing audit documentation for an audit of financial statements.

E

because the auditor obtains audit evidence at each stage.

Açıklama:

Auditor uses audit sampling in performing audit procedures. He/she deals with the use of statistical or

non-statistical sampling when he/she designs and selects the audit sample, performs tests of controls and

tests of details and evaluates the results from the sample (Şavlı, 2019, p. 124-126). Therefore, the auditor

cannot guarantee 100% correctness of financial statements because the audit opinion is based on the audit

evidence obtained through audit sampling. This is another reason why the auditor’s audit opinion is based

on reasonable assurance.

The auditor cannot guarantee 100% correctness because his/her findings are based on evidence selected through audit sampling.

non-statistical sampling when he/she designs and selects the audit sample, performs tests of controls and

tests of details and evaluates the results from the sample (Şavlı, 2019, p. 124-126). Therefore, the auditor

cannot guarantee 100% correctness of financial statements because the audit opinion is based on the audit

evidence obtained through audit sampling. This is another reason why the auditor’s audit opinion is based

on reasonable assurance.

The auditor cannot guarantee 100% correctness because his/her findings are based on evidence selected through audit sampling.

Soru 10

Which of the following is not one of the sub-stages of the reporting stage?

Seçenekler

A

Evaluate results

B

Perform additional tests

C

Accumulate final evidence

D

Issue audit report

E

Perform test of controls

Açıklama:

Perform additional tests for presentation and disclosure

Accumulate final evidence

Evaluate results

Issue audit report

are the substages of reporting stage.

Perform test of controls is not sub stage of reporting.

Accumulate final evidence

Evaluate results

Issue audit report

are the substages of reporting stage.

Perform test of controls is not sub stage of reporting.

Soru 11

Which of the following fundamental principles of ethics refer to being straightforward and honest in all professional and business relationships?

Seçenekler

A

Objectivity

B

Professional competence and due care

C

Confidentiality

D

Integrity

E

Professional behavior

Açıklama:

Integrity refers to being straightforward and honest in all professional and business relationships. The answer is D.

Soru 12

- Inherent Risk

- Sampling Risk

- Control Risk

Seçenekler

A

Only I

B

I and II

C

I and III

D

II and III

E

I, II and III

Açıklama:

Risk of material misstatement is the risk that financial statements are materially misstated prior

to audit. It is generated from the client firm. The auditor has no effect on it. It has two components, namely inherent risk and control risk. The answer is C.

to audit. It is generated from the client firm. The auditor has no effect on it. It has two components, namely inherent risk and control risk. The answer is C.

Soru 13

Which of the following is not one of the transaction-related audit objectives?

Seçenekler

A

Occurrence

B

Completeness

C

Accuracy

D

Classification

E

Existence

Açıklama:

Transaction-related audit objectives are:

• Occurrence: The auditor will check whether recorded transactions have actually occurred.

• Completeness: The auditor will check whether all transactions that should be included in the

journals have actually been included.

• Accuracy: The auditor will check whether recorded transactions are stated at the correct amounts.

• Posting and summarization: The auditor will check whether recorded transactions are properly

included in the master files and are correctly summarized.

• Classification: The auditor will check whether transactions included in the client firm’s general

journals are properly classified.

The answer is E.

• Occurrence: The auditor will check whether recorded transactions have actually occurred.

• Completeness: The auditor will check whether all transactions that should be included in the

journals have actually been included.

• Accuracy: The auditor will check whether recorded transactions are stated at the correct amounts.

• Posting and summarization: The auditor will check whether recorded transactions are properly

included in the master files and are correctly summarized.

• Classification: The auditor will check whether transactions included in the client firm’s general

journals are properly classified.

The answer is E.

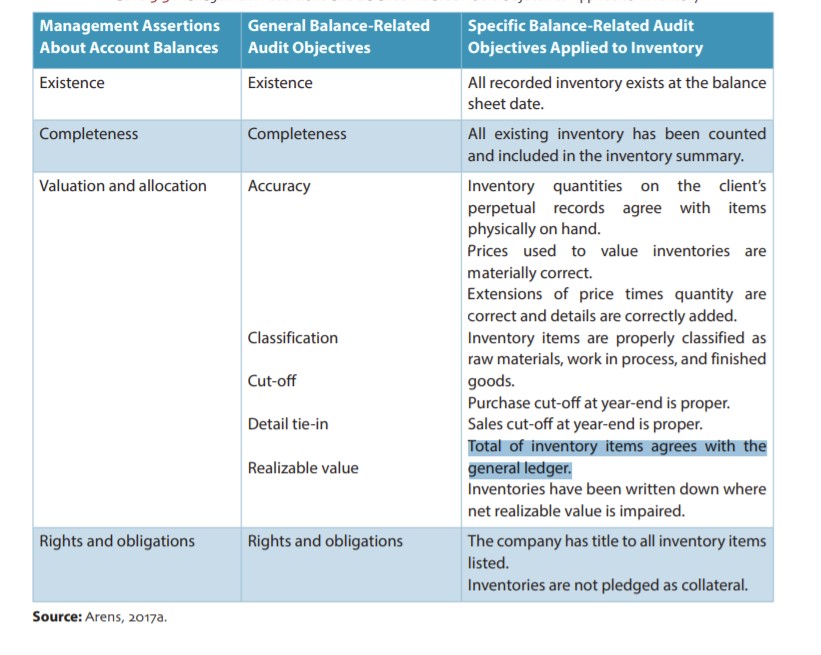

Soru 14

Which of the following balance-related audit objectives is related to checking whether transactions are recorded and included in account balances in the proper period?

Seçenekler

A

Cutoff

B

Detail tie-In

C

Realizable Value

D

Rights and Obligations

E

Classification

Açıklama:

Balance-related audit objectives focus on not only verification of the account balance but also verification of the detail that supports the account balance. There are eight general balance-related objectives as follows: existence, completeness, accuracy, classification, cut off, detail tie-in, realizable value, and rights and obligations.

The answer is A.

- Existence: The auditor will check whether the amounts included in the financial statements should actually be included.

- Completeness: The auditor will check whether all amounts that should be included have actually been included.

- Accuracy: The auditor will check whether amounts included are stated at the correct amounts.

- Classification: The auditor will check whether amounts included in the client’s listing are properly classified.

- Cutoff: The auditor will check whether transactions are recorded and included in account balances in the proper period.

- Detail tie-In: The auditor will check the details on lists are accurately prepared, correctly added, and agree with the general ledger.

- Realizable Value: The auditor will check whether an account balance has been reduced for declines from historical cost to net realizable value or when accounting standards require fair market value accounting treatment.

- Rights and Obligations: Most assets must be owned before it is acceptable to include them in the financial statements. Similarly, liabilities must belong to the entity. Rights are always associated with assets and obligations with liabilities. The auditor will check whether assets and liabilities are listed.

The answer is A.

Soru 15

Which of the following terms is about the information used by the auditor in arriving at the conclusions on which the auditor’s opinion is based?

Seçenekler

A

Audit objectives

B

Risk assessment procedures

C

Audit evidence

D

Management assertions

E

Financial statement

Açıklama:

Audit evidence is the information used by the auditor in arriving at the conclusions on which the

auditor’s opinion is based. The answer is C.

auditor’s opinion is based. The answer is C.

Soru 16

Which of the following is not one of the audit techniques that the auditor benefits from when obtaining appropriate audit evidence?

Seçenekler

A

Inspection

B

Detail tie-in

C

Recalculation

D

Inquiry

E

External Confirmation

Açıklama:

In order to obtain sufficient appropriate evidence and to form an audit opinion, the auditor usually

benefits from the following seven audit techniques (ISA 500.A14-A25). These are inspection, observation, external confirmation, recalculation, inquiry, reperformance and analytical procedures. Detail tie-in is one of the managerial assertions. The answer is B.

benefits from the following seven audit techniques (ISA 500.A14-A25). These are inspection, observation, external confirmation, recalculation, inquiry, reperformance and analytical procedures. Detail tie-in is one of the managerial assertions. The answer is B.

Soru 17

- preparation of the audit plan

- the evaluation of the audit evidence obtained,

- forming an audit opinion

- understanding of the client firm’s business and industry

- preparation of the audit report

Seçenekler

A

I, II, IV

B

III, IV, V

C

I, III

D

II, IV, V

E

I, IV

Açıklama:

The risk assessment involves 1) the client acceptance or continuance, 2) understanding of the client firm’s business and 3) industry and preparation of the audit plan.

Risk response involves the processes of obtaining audit evidence.

Reporting involves 1) the evaluation of the audit evidence obtained, 2) forming an audit opinion and 3) preparation of the audit report.

The answer is E.

Risk response involves the processes of obtaining audit evidence.

Reporting involves 1) the evaluation of the audit evidence obtained, 2) forming an audit opinion and 3) preparation of the audit report.

The answer is E.

Soru 18

Which of the following terms refers to the magnitude of misstatements that could reasonably be expected to influence the economic decisions of users made based on the financial statements?

Seçenekler

A

Internal control

B

External Control

C

Analytical procedures

D

Materiality

E

Managerial assertions

Açıklama:

Materiality is the magnitude of misstatements that could reasonably be expected to influence the economic decisions of users made based on the financial statements. The answer is D.

Soru 19

Which of the following terms refers to a set of policies and procedures determined to achieve objectives of the client firm’s management related to financial reporting, operations and compliance?

Seçenekler

A

Materiality

B

Audit

C

External control

D

Inherent risk

E

Internal control

Açıklama:

Internal control is a set of policies and procedures determined to achieve objectives of the client firm’s management related to financial reporting, operations and compliance. The answer is E.

Soru 20

Which of the following is implemented to assess the overall reasonableness of transactions and balances?

Seçenekler

A

Tests of details of balances

B

Substantive analytical procedures

C

Substantive tests of transactions

D

Tests of controls

E

Performance materiality

Açıklama:

Substantive analytical procedures assess the overall reasonableness of transactions and balances. The answer is B.

Ünite 4

Soru 1

Why must the proposal for auditing engagement come from the client?

Seçenekler

A

because the auditing firm cannot advertise itself.

B

because it is risky otherwise.

C

because accuracy is the most important part of the process.

D

because otherwise the auditing firm cannot be independent.

E

because client secrecy is very important.

Açıklama:

Due to the nature of the auditing profession, auditors cannot engage in advertising activities to receive proposals. The proposal must come from

the client. The proposal received by the audit firm is first evaluated by the managers of the audit firm, and then, if the parties agree, then the engagement phase is started.

The proposal for auditing engagement must come from the client because the auditing firm cannot advertise itself.

the client. The proposal received by the audit firm is first evaluated by the managers of the audit firm, and then, if the parties agree, then the engagement phase is started.

The proposal for auditing engagement must come from the client because the auditing firm cannot advertise itself.

Soru 2

Which of the following is one of the objectives of the auditor to

benefit from ARPs?

benefit from ARPs?

Seçenekler

A

To understand the business and the sector in which it operates

B

To compare business data with expected results determined by the auditor

C

To consider fraud risk throughout the entire audit work

D

To compare the data of the business with expected results

E

To assess the client’s business risk and to get to know

the business better.

the business better.

Açıklama:

The objectives of the auditor to

benefit from ARPs are:

• To understand the business and the sector

in which it operates,

To understand the business and the sector in which it operates is an objective of the auditor from the ARP.

benefit from ARPs are:

• To understand the business and the sector

in which it operates,

To understand the business and the sector in which it operates is an objective of the auditor from the ARP.

Soru 3

Which of the following is not among the objectives of the auditor to

benefit from ARPs?

benefit from ARPs?

Seçenekler

A

To understand the business and the sector

in which it operates

in which it operates

B

To reduce the number of detailed tests

C

To attract management’s attention to expected misstatements

D

To evaluate the sustainability (continuity) of the business

E

to recognize the relationship of business and fraud risks with the

financial statements

financial statements

Açıklama:

The objectives of the auditor to

benefit from ARPs are:

• To understand the business and the sector

in which it operates,

• To evaluate the sustainability (continuity)

of the business,

• Attracting management’s attention to

expected misstatements,

• To reduce the number of detailed tests.

To recognize the relationship of business and fraud risks with the

financial statements is not an objective of ARPs.

benefit from ARPs are:

• To understand the business and the sector

in which it operates,

• To evaluate the sustainability (continuity)

of the business,

• Attracting management’s attention to

expected misstatements,

• To reduce the number of detailed tests.

To recognize the relationship of business and fraud risks with the

financial statements is not an objective of ARPs.

Soru 4

What is the minimum number of team members in an audit team?

Seçenekler

A

1

B

2

C

3

D

4

E

5

Açıklama:

According to ISA, it is obligatory to form an

audit team consisting of six persons, at least three

originals and three backups, for each audit work.

Therefore, each audit is carried out by a team

of auditors. The size of this team is determined

according to the number and quality required by

the job, and it cannot be less than three auditors.

three members is the minimum. 6 members with three originals and three backups is the usual.

audit team consisting of six persons, at least three

originals and three backups, for each audit work.

Therefore, each audit is carried out by a team

of auditors. The size of this team is determined

according to the number and quality required by

the job, and it cannot be less than three auditors.

three members is the minimum. 6 members with three originals and three backups is the usual.

Soru 5

Which of the following statements is not true about audit risk assessment?

Seçenekler

A

The auditor wishes to keep the AR level low.

B

The auditor wishes to express an unqualified opinion.

C

A zero of AR means absolute (100%) assurance.

D

If AR is 2%, the confidence level of the audit is 98%.

E

Audit risk (AR) is the possibility of encountering significant misstatements in the financial statements.

Açıklama:

Audit risk (AR) is the

possibility of encountering significant misstatements in the financial statements, although the audit has

been completed and an unqualified opinion is issued. The auditor wishes to keep the AR level low, that

is, the auditor wishes not to express an unqualified opinion, although the financial statements contain

material misstatements. A zero of AR means absolute (100%) assurance which is economically impossible.

AR also tells the level of confidence of an audit. For example, if AR is 2%, the confidence level of the audit

is 98%.

The auditor wishes not to express an unqualified opinion.

possibility of encountering significant misstatements in the financial statements, although the audit has

been completed and an unqualified opinion is issued. The auditor wishes to keep the AR level low, that

is, the auditor wishes not to express an unqualified opinion, although the financial statements contain

material misstatements. A zero of AR means absolute (100%) assurance which is economically impossible.

AR also tells the level of confidence of an audit. For example, if AR is 2%, the confidence level of the audit

is 98%.

The auditor wishes not to express an unqualified opinion.

Soru 6

If the risk exists because of the the existence of related parties, foreign partners, complex agreements, what kind of risk is it regarded as?

Seçenekler

A

Inherent risk

B

Control risk

C

Detection risk

D

Acceptable audit risk

E

Account risk

Açıklama:

Inherent Risk: It is the

evaluation of the probability of

material misstatements in an account

balance or a class of transaction,

regardless of the effectiveness of the

internal control structure. Some

sectors are riskier than in other

sectors. The existence of related

parties, foreign partners, complex

agreements provide grounds for

misstatements. Similarly, some

accounts and transactions may have

more inherent risks than others.

Inherent risk is the answer.

evaluation of the probability of

material misstatements in an account

balance or a class of transaction,

regardless of the effectiveness of the

internal control structure. Some

sectors are riskier than in other

sectors. The existence of related

parties, foreign partners, complex

agreements provide grounds for

misstatements. Similarly, some

accounts and transactions may have

more inherent risks than others.

Inherent risk is the answer.

Soru 7

" _______________ is the maximum amount of misstatement that the auditor can accept."

Which of the following could best fill in the blank in the statement above?

Which of the following could best fill in the blank in the statement above?

Seçenekler

A

the tolerable misstatement level

B

the level of materiality

C

preliminary materiality level

D

the volume of the client business

E

account balance anomaly

Açıklama:

the tolerable misstatement level is the maximum amount of

misstatement that the auditor can accept.

misstatement that the auditor can accept.

Soru 8

Which of the following statements about the distinction between control and audit is not true?

Seçenekler

A

Control is an issue that comes before the audit and should be considered more broadly.

B

While control is a continuous activity, the audit is carried out in a certain period.

C

While the control is carried out simultaneously, the audit is retroactive.

D

While mechanical tools can be used in the control, the audit is carried out by people.

E

While it is not necessary to be independent of the company in the audit, independence is essential in the control.

Açıklama:

While it is not necessary to be independent

of the company in the control, independence

is essential in the audit.

of the company in the control, independence

is essential in the audit.

Soru 9

Which of the following is not one of the primary goals of the internal control system for a business?

Seçenekler

A

Increasing the reliability of the company

B

Ensuring compliance with legislation

C

Providing accurate and timely financial reporting

D

Contributing to operational efficiency

E

Getting familiarized with the ICS of the client business

Açıklama:

Internal controls serve four primary purposes in

a business. These are:

• Increasing the reliability of the company,

• Ensuring compliance with the legislation,

• Providing accurate and timely financial

reporting,

• Contributing to operational efficiency.

E is related to auditor not business company.

a business. These are:

• Increasing the reliability of the company,

• Ensuring compliance with the legislation,

• Providing accurate and timely financial

reporting,

• Contributing to operational efficiency.

E is related to auditor not business company.

Soru 10

Which of the following is not one of the shortcomings of SMEs in Turkey for running Internal Control Systems?

Seçenekler

A

Institutionalism

B

Risk management

C

Written policies and procedures

D

Performance measurement

E

Collection of evidence

Açıklama:

SMEs in Turkey, an advanced ICS is not yet able to be implemented. The main encountered

shortcomings are:

• Institutionalization

• Risk management

• Written policies and procedures (Business processes)

• Performance measurement (predominantly

financial criteria)

• Principle of segregation of duties and

authorization

• IFRS competence

• Periodic control activities (such as regular

inventory count)

• Information security

• Internal audit function

• Some deficiencies in the reporting and

budgeting system,

• Deficiencies in information systems.

Collection of evidence is not a shortcoming of SMEs in terms of ICS.

shortcomings are:

• Institutionalization

• Risk management

• Written policies and procedures (Business processes)

• Performance measurement (predominantly

financial criteria)

• Principle of segregation of duties and

authorization

• IFRS competence

• Periodic control activities (such as regular

inventory count)

• Information security

• Internal audit function

• Some deficiencies in the reporting and

budgeting system,

• Deficiencies in information systems.

Collection of evidence is not a shortcoming of SMEs in terms of ICS.

Soru 11

I. Experienced team members should be involved in the assessment

II. Professional self-reliance

III. Professional skepticism

IV. Professional judgement

Which of the above are some of the requirements for success at the risk assessment phase?

II. Professional self-reliance

III. Professional skepticism

IV. Professional judgement

Which of the above are some of the requirements for success at the risk assessment phase?

Seçenekler

A

I, II, III and IV

B

I, II and IV

C

I, III and IV

D

II and IV

E

III and IV

Açıklama:

The auditor must meet the following requirements to be successful at the risk assessment phase.

The right answer is B.

- Experienced team members should be involved in the assessment,

- Professional skepticism,

- Planning,

- Communication between team members,

- Focus on determining the risk,

- Assessment of management’s approaches to risk (such as internal controls),

- Professional judgment.

The right answer is B.

Soru 12

I. Inherent Risk (IR)

II. Control Risk (CR)

III. Detection Risk (DR)

Which of the following is/are related to “risk of material misstatement” ?

II. Control Risk (CR)

III. Detection Risk (DR)

Which of the following is/are related to “risk of material misstatement” ?

Seçenekler

A

Only I

B

I and II

C

I, II and III

D

I and III

E

Only III

Açıklama:

Audit risk components, or in other words, the audit risk model includes three different types of risks. These are a) Inherent Risk (IR), b) Control Risk (CR) and c) Detection Risk (DR). Audit risk is found by multiplying these three types of risk probabilities. According to ISA 315; The inherent risk and control risk related to the client’s business from these risks is called “risk of material misstatement”. The answer is B .

Soru 13

Which of the following are the steps in auditor’s actions during the auditing process?

Seçenekler

A

Accepting the engagement and arrangement, Audit planning, Performing audit procedures, and Reporting of findings.

B

Accepting the engagement, Risk Assessment, Responding to the risk, and Reporting.

C

Accepting the engagement and arrangement, Risk assessment, Audit planning, and Reporting

D

Accepting the engagement and arrangement, Risk assessment, Audit planning, and Reporting of findings.

E

Risk Assessment, Responding to the risk, and Reporting.

Açıklama:

The auditor ‘s actions can be classified in four steps during the audit process. That are like the following:

Accepting the engagement and arrangement, Audit planning, Performing audit procedures, and Reportingof findings. The conventional audit approach was discarded at the beginning of the 2000s, with the advent of large-scale financial scandals (Enron and Worldcom in the US, Parmalat in Italy and Imar Bank in Turkey), and a ‘risk-based’ approach began to be embraced. Therefore, the audit process turns into another three phases in this approach (also referred to as 3R Audit). These are: Risk Assessment, Responding to the risk, and Reporting. The Answer is A

Accepting the engagement and arrangement, Audit planning, Performing audit procedures, and Reportingof findings. The conventional audit approach was discarded at the beginning of the 2000s, with the advent of large-scale financial scandals (Enron and Worldcom in the US, Parmalat in Italy and Imar Bank in Turkey), and a ‘risk-based’ approach began to be embraced. Therefore, the audit process turns into another three phases in this approach (also referred to as 3R Audit). These are: Risk Assessment, Responding to the risk, and Reporting. The Answer is A

Soru 14

I. Misappropriation of assets

II. Fraudulent financial reporting

III. Corruption

IV. Surveillance

Which of the above are frauds encountered in businesses?

II. Fraudulent financial reporting

III. Corruption

IV. Surveillance

Which of the above are frauds encountered in businesses?

Seçenekler

A

I, II and III

B

I, II and IV

C

I, II, III and IV

D

I and III

E

I, III and IV

Açıklama:

Frauds in businesses are classified into three groups:

The answer is A

- Misappropriation of assets (also called employee fraud)

- Fraudulent financial reporting

- Corruption

The answer is A

Soru 15

I. Planning will help the auditor gather sufficient and appropriate evidence to form an opinion

II. Planning will help the auditor perform the audit at an affordable cost.

III. Planning is a continuous and repetitive process.

IV. Planning will help the auditor avoid misunderstandings about the business

V. Planning is a one-time job

Which of the above can be said related to planning?

II. Planning will help the auditor perform the audit at an affordable cost.

III. Planning is a continuous and repetitive process.

IV. Planning will help the auditor avoid misunderstandings about the business

V. Planning is a one-time job

Which of the above can be said related to planning?

Seçenekler

A

I, II,III and IV

B

I, II, III and V

C

I, II, III, IV and V

D

II, III and IV

E

II, III, IV and V

Açıklama:

Planning will help the auditor gather sufficient and appropriate evidence to form an opinion, perform the audit at an affordable cost, and avoid misunderstandings about the business. Planning is a continuous and repetitive process. The answer is A

Soru 16

Which of the following are related to scope in the creation of audit strategy ?

Seçenekler

A

the level of materiality

B

highrisk areas

C

internal control

D

the provision of other services

E

places to visit

Açıklama:

The matters to be considered in the creation of audit strategy are: Scope of the engagement: Specific features of the sector, financial reporting framework, places to visit, utilization of the internal auditor’s work, the impact of information technologies, relations with group companies. Audit schedule and communication structure: Reporting times of the client business, meeting times with business representatives and team members, meetings between the team members and third parties. Identification of important factors related to the audit: the level of materiality, highriskareas, internal control, the auditor’ s professional skepticism, the results of previous audits, and the provision of other services. The answer is E.

Soru 17

I. Control is an issue that comes before the audit and should be considered more broadly.

II. While control is a continuous activity, the audit is carried out in a certain period.

III. While the control is carried out simultaneously, the audit is retroactive.

IV. Control and the audit is carried out by people.

V. Independence is essential in control and the audit.

Which of the above are true about the differences between control and audit?

II. While control is a continuous activity, the audit is carried out in a certain period.

III. While the control is carried out simultaneously, the audit is retroactive.

IV. Control and the audit is carried out by people.

V. Independence is essential in control and the audit.

Which of the above are true about the differences between control and audit?

Seçenekler

A

I, II and III

B

I, III and IV

C

I, III, IV and V

D

I, III and V

E

IV and V

Açıklama:

Control is an issue that comes before the audit and should be considered more broadly.

The answer is A

- While control is a continuous activity, the audit is carried out in a certain period.

- While the control is carried out simultaneously, the audit is retroactive.

- While mechanical tools can be used in the control, the audit is carried out by people.

- While it is not necessary to be independent of the company in the control, independence is essential in the audit.

The answer is A

Soru 18

The probability of an auditor to miss misstatements in the financial statements of the client’s business with the collected audit evidence (regarding the account balances) is called by which of the following?

Seçenekler

A

Controlled Dedection Risk

B

Planned Detection Risk

C

İnherent Risk

D

Audit Risk

E

Acceptable Audit Risk

Açıklama:

Control Risk: CR is a function of the effectiveness of the internal control designed for financial reporting. It is the auditor’s assessment of the probability of failure in the client’s business internal controls to prevent or reveal the misstatements in an account balance or class of transaction that exceed the acceptable limit.

Inherent Risk: It is the evaluation of the probability of material misstatements in an account balance or a class of transaction, regardless of the effectiveness of the internal control structure.

Detection Risk: The probability of an auditor to miss misstatements in the financial statements of the client’s business with the collected audit evidence (regarding the account balances) is called “Detection Risk” or “Planned Detection Risk”.

The answer is B .

Inherent Risk: It is the evaluation of the probability of material misstatements in an account balance or a class of transaction, regardless of the effectiveness of the internal control structure.

Detection Risk: The probability of an auditor to miss misstatements in the financial statements of the client’s business with the collected audit evidence (regarding the account balances) is called “Detection Risk” or “Planned Detection Risk”.

The answer is B .

Soru 19

Which of the following is not related to Control Environment?

Seçenekler

A

It consists of procedures that reflect the attitudes of the senior managers

B

It consists of partners regarding the internal control system and importance given to it

C

It has a widespread effect

D

Goals should be set in the context of an organizational strategy,

E

The culture and history of the organization directly affect the control environment

Açıklama:

Risk Assessment: All organizations face risks threatening to reach its targets. All internal and external risks should be evaluated. Prerequisite for risk assessment is the determination of different but interrelated targets within the business. Risks should be assessed and managed accordingly.

Setting clear goals is essential to recognize, evaluate, and respond to risks. Creating a set of goals can be quite formal or informal. Goals should be set in the context of an organizational strategy, considering the strengths and weaknesses, risks, and opportunities of the company.

Internal controls help reduce risks in achieving the goals set in a business but do not eliminate all risks. The auditor collects information on how management assesses risks specifically for financial reporting, through questionnaires and interviews. The answer is D.

Setting clear goals is essential to recognize, evaluate, and respond to risks. Creating a set of goals can be quite formal or informal. Goals should be set in the context of an organizational strategy, considering the strengths and weaknesses, risks, and opportunities of the company.

Internal controls help reduce risks in achieving the goals set in a business but do not eliminate all risks. The auditor collects information on how management assesses risks specifically for financial reporting, through questionnaires and interviews. The answer is D.

Soru 20

I. Control environment

II. Risk assessment

III. Control activities

IV. Information and communication

V. Monitoring activities

Which of the above are the components of internal control according to the COSO report?

II. Risk assessment

III. Control activities

IV. Information and communication

V. Monitoring activities

Which of the above are the components of internal control according to the COSO report?

Seçenekler

A

I, II , III and IV

B

I, II and IV

C

I, II, III, IV and V

D

II, III and IV

E

II, IV and V

Açıklama:

Internal Control Components

Control environment,

Risk assessment,

Control activities,

Information and communication,

Monitoring activities. The answer is C

Control environment,

Risk assessment,

Control activities,

Information and communication,

Monitoring activities. The answer is C

Ünite 5

Soru 1

- Know specific audit objectives for classes of transactions, accounts, and disclosures

- Divide financial statements into cycles

- Understand objectives and responsibilities for the audit

- Know management assertions about financial statements

- Know general audit objectives for classes of transactions, accounts, and disclosures

Seçenekler

A

II

B

III

C

IV

D

I

E

V

Açıklama:

The five steps to develop audit objectives are:

- Understand objectives and responsibilities for the audit

- Divide financial statements into cycles

- Know management assertions about financial statements

- Know general audit objectives for classes of transactions, accounts, and disclosures

- Know specific audit objectives for classes of transactions, accounts, and disclosures

Soru 2

Which of the followings is NOT one of the management assertions related to account balances and related disclosures, at the period end?

Seçenekler